Is China an Emerging Market?

Is China an Emerging Market?

China has been viewed as an emerging market over the past several decades, although its current status is not as straightforward as you might expect. Many index providers classify China as an emerging market, although the economic and investment reality is more complex. China has displays many characteristics of emerging markets, yet is is the second largest economy in the world (which adds complexity to the debate).

In recent years, China has experienced remarkable economic growth and its economy is larger than any other country except the US. Yet, this remarkable development has not entirely erased some attributes typical of emerging markets, such as weaker regulatory systems and disparate income levels. Observers should be mindful of the nuances and intricacies that come with its unique position in the global landscape. Exploring this topic is vital in comprehending China’s role in today’s world economy and how it might evolve in the future.

Is China an Emerging Market?

Anyone exploring the question of whether China is an emerging market must consider the characteristics of both emerging and developed markets. Factors including economic growth, per capita GDP, and market accessibility play crucial roles in determining a country’s status as an emerging or developed market.

On the one hand, China’s rapid economic growth and influence on the global market have captured attention. According to a Pew Research Center survey, public opinion in emerging markets largely has a positive view of China’s economic stature, with many believing that China’s growing economy benefits their countries. Additionally, China’s stock market has become more open to the global financial system, attracting international investors.

Despite these impressive strides, China’s GDP per capita remains relatively low compared to developed markets at $12,556 (according to the World Bank). This level of GDP per capita supports China’s status as an emerging market in classifications like the Morgan Stanley Capital International (MSCI) indices.

However, as the line between emerging and developed markets blurs, it’s important to recognize that China’s economic situation defies conventional labels. The sheer size of China’s markets and influence on the global economy challenges traditional analysis frameworks.

Many commenters overgeneralize or exaggerate claims rather than speak to the complexity and evolving nature of China’s economy.

Economic Growth and Development

Size of Economy

One of the key indicators to consider is the size of China’s economy. China has experienced remarkable growth in recent decades and is now the second-largest economy in the world, following the United States. That does not square with the “emerging” label.

Industrialization

Another factor that influences the classification of China as an emerging market is industrialization. Over the years, China has transitioned from a predominantly agricultural economy to a major global manufacturing hub. The country has seen rapid expansion in various industries, including automobile production, electronics, and renewable energy. Consequently, this has led to increased exports and a strong industrial base, which is more typical of an emerging market than a developed market which typically has a lot of domestic consumption and more a more services-based economy.

Urbanization

Finally, urbanization plays a crucial role in determining China’s position in the global economic landscape. As more people move from rural areas to cities, there is a rise in demand for infrastructure, housing, and other amenities. This urban migration has facilitated the rapid development of urban centers, boosting economic growth along with it. This shift is consistent with countries moving from an emerging to a developed classification.

By examining these aspects, it becomes clear that China exhibits both characteristics of emerging and developed markets, making it difficult to definitively label it as either.

Market Structure

Market Capitalization

As you explore the market structure of China, it’s important to consider market capitalization. According to the World Bank, China has one of the largest stock markets in the world with a market capitalization of around $12.2 trillion (again, second only to the US with $40.7T). Again, I am not sure a country with the second largest market cap in the world can be considered emerging.

Fixed vs Floating Currency

Another aspect to take into account when examining China’s market structure is its currency system. China has a managed exchange rate, which means the value of its currency, the renminbi (RMB), is not determined solely by market forces. The People’s Bank of China (PBOC) intervenes in the foreign exchange market to manage the value of the RMB, which contrasts with the purely floating exchange rates used by most developed countries.

State-Owned Enterprises

Lastly, an important characteristic of China’s market structure is the presence and influence of state-owned enterprises (SOEs). SOEs continue to play a significant role in the Chinese economy, dominating strategic industries like energy, finance, and telecommunications. While the government has initiated various reforms to open up the markets and encourage private sector growth, SOEs still account for a substantial portion of China’s GDP and employment. In comparison, state-owned enterprises have a lesser presence in developed markets, where the private sector primarily drives the economy.

China exhibits a mix of characteristics from both emerging and developed markets. Its market capitalization has grown tremendously but remains smaller than major developed markets, it uses a managed exchange rate system unlike the purely floating rates of most advanced economies, and state-owned enterprises hold a significant presence in the economy, differing from the private sector-centric structure in developed markets.

Challenges Facing China’s Economy

Rule of Law

In addressing the challenges facing China’s economy, it’s important to consider the role of the rule of law. Weaknesses in legal infrastructure and unequal enforcement of existing laws can hinder growth and foster corruption. The existing situation in China appears to much more consistent with an emerging market rather than a developed one.

Inequality

Rapid industrialization and urbanization have lifted millions out of poverty, but gaps in income distribution persist. Rural and urban areas can show stark differences in wealth and development, with disparities in access to education, healthcare, and other social services.

Environmental Issues

Rapid industrialization and urbanization have also led to widespread air, water, and soil pollution. To promote long-term, sustainable development, the Chinese government has started implementing environmental protection policies, such as stricter regulations on emissions and waste disposal and increased investment in renewable energy and clean technologies

Implications for the Global Economy

Trade Relations

As China continues to grow, its influence on global economic trends and trade relations will likely expand. China’s rise as a key player in the world economy has led to stronger trade ties with various countries. This has boosted economic growth in many emerging markets, while also creating new opportunities for trade and investment.

However, it is essential to keep in mind that there may be challenges associated with China’s growing influence on trade relations. These challenges could arise from trade disputes, intellectual property concerns, and local industries’ competitive pressures.

Economic Growth and International Development

China’s massive economic growth has had a rippling effect on other emerging economies. In particular, its investment in infrastructure and resources in developing countries has helped stimulate growth and reduce poverty in various regions. As China’s economy continues to thrive, you can expect an increase in its investments in several high-growth sectors, such as technology, clean energy, and manufacturing. Very few emerging markets (or even developed ones!) provide the level of foreign aid and investment that China does.

Global Governance and Security

China’s rise in the global economy has also brought about changes in international governance and security. China is increasingly taking an influential role in global institutions which may lead to shifts in international policies and norms. Moreover, China is gradually building up its military capabilities to assert its regional and global security interests.

Given China’s mix of emerging and developed market characteristics, its growing role in the global economy has numerous implications for trade relations, economic growth, and international governance.

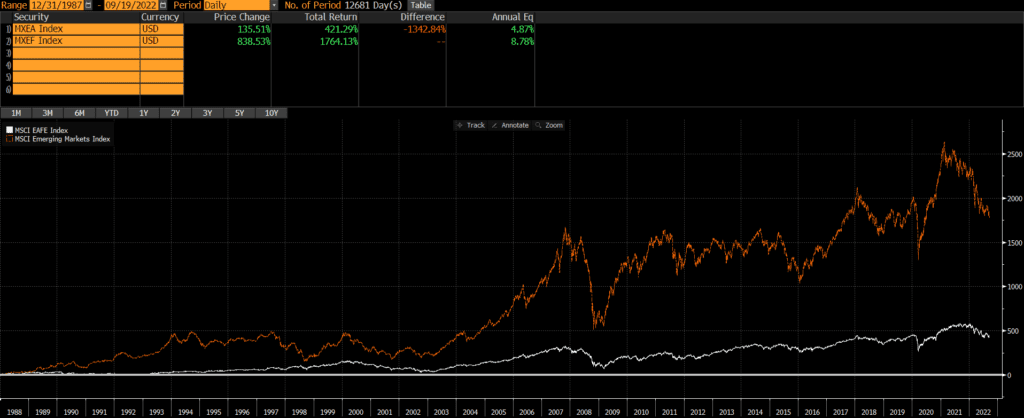

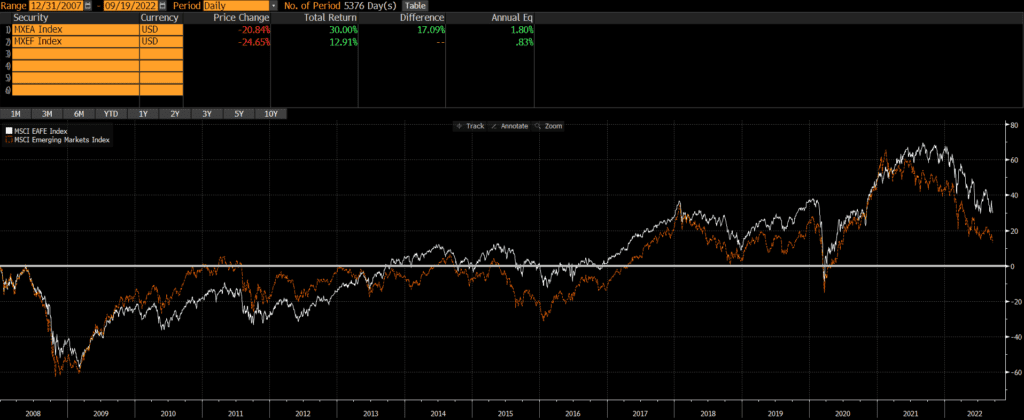

China’s Role in the Emerging Market Index

China is by far the largest constituent in the major emerging market indices, although its weight fluctuates with global stock markets. Even Chinese debt is becoming more prominent in investor portfolios.

It’s also worth noting the changes in index methodology. In 2019, MSCI increased the inclusion ratio of China A shares in its Emerging Markets Index. This development has led global investors to re-evaluate their equity portfolio allocation frameworks, considering China’s growing economic strength and improving market accessibility.

Conclusion

In determining whether China is an emerging market, we must consider its unique characteristics which straddle the line between developed and developing economies. As the world’s second-largest economy and a key player in global trade, China has established itself as an influential participant in both advanced and emerging markets. On the other hand, it’s important to recognize that the country continues to face certain challenges typically associated with emerging markets.

Rather than relying on the index provider’s classification of China as an emerging market, I believe it is best to embrace the idea that China exhibits characteristics of both emerging and developed nations. By appreciating its multi-faceted nature and evolving economic relationships, we can gain a more nuanced understanding of China’s position in the global market landscape.