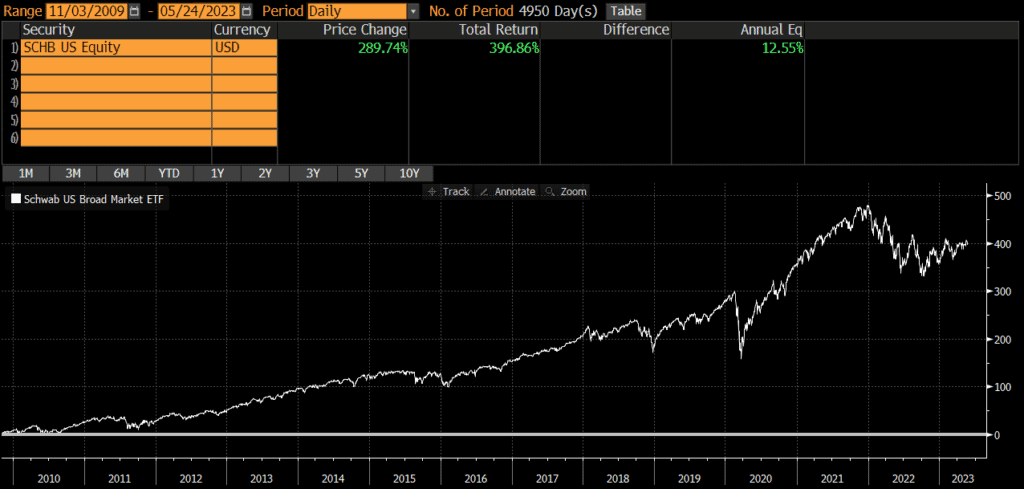

The Schwab US Broad Market ETF (symbol: SCHB) is one of the largest exchange-traded funds (ETFs) in the market and widely used by both individual and institutional investors. SCHB is a low-cost index fund, which tracks the Dow Jones US Broad Stock Market Index. As its name implies, it seeks to provide exposure to the broad US stock market at a very low price. The fund is the core of many portfolios and the below review of SCHB will evaluate why that is.

The first thing most investors want to know about is performance, so we will start there. According to Bloomberg, since the fund’s inception 14 years ago, SCHB has returned over 12.5% per year. Of course, this figure can go up or down and the returns in any single year are unlikely to be 12.5%. From 2010 through 2022 (13 years), SCHB was up in 11 years and down in 2 years. The average return in the up years was 17.5%, while the average return in the down years was -12.4%.

Source: ThoughtfulFinance.com, Bloomberg

SCHB Risks

SCHB owns stocks which are more volatile than cash or bonds. While the returns are higher than cash or bonds, investors need to be prepared to stomach volatility and be able to hold for the longer-term. SCHB was down over 35% during the covid pandemic and similar funds declined roughly 50% during the previous two recessions in 2001 and 2007. This is not necessarily worse than other similar funds, but it is a characteristic of stocks that investors need to be aware of.

SCHB Portfolio

Fund performance is ultimately driven by a fund’s holdings and exposures, so our SCHB review will examine these items.

SCHB Holdings

SCHB (and its underlying index) is incredibly diversified, holding nearly 4,000 stocks. This represents the vast majority of the US stock market.

SCHB

Dow Jones US Broad Stock Market Index

Number of Stocks

2,484

2,519

Sources: ThoughtfulFinance.com, Schwab (as of 3/31/2023)

SCHB Country Exposures

SCHB only owns US-based companies. Investors looking for international exposure may pair SCHB with international ETFs or simply hold a global ETF.

SCHB Market Cap Exposure

SCHB is a “total market” fund which seeks to represent the entire US stock market, which is predominantly composed of large-caps. Even though the fund holds mid-caps and small-caps, performance is primarily driven by the large-cap exposure. This dynamic can be found by comparing SCHB to SWPPX (a large-cap fund).

SCHB

Large-Cap

73%

Mid-Cap

19%

Small-Cap

8%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/24/2023

SCHB Sector Exposures

SCHB is extremely diversified across sectors and mirrors the approximate weights of the broad US stock market.

SCHB

Basic Materials

2.47%

Consumer Cyclical

10.61%

Financial Services

12.53%

Real Estate

3.14%

Communication Services

8.04%

Energy

4.40%

Industrials

8.98%

Technology

26.69%

Consumer Defensive

6.49%

Healthcare

14.01%

Utilities

2.65%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/24/2023

Expenses

No review of SCHB would be complete without an in-depth look at the explicit and implicit costs of trading and holding SCHB.

SCHB Expense Ratio

SCHB’s expense ratio of .03% is among the lowest of any total market funds. Even if another fund is free, three basis points is not a material difference in my opinion.

SCHB Transaction Costs

ETFs are free to trade at many brokers and custodians, so SCHB should be free to trade in most cases. Additionally, it is among the largest ETFs and is very liquid. The bid-ask spread of SCHB is about .01%, so individual investor trades will not generally be large enough to impact or move the market.

SCHB Tax Efficiency

Like most index funds, SCHB is very tax-efficient. Unlike actively-managed funds, passively-managed index funds typically have less trading and lower turnover. This results in fewer taxable events and higher tax efficiency.

ETFs are typically more tax-efficient than mutual funds, due to their ability to avoid realizing capital gains through like-kind redemptions (a process that is beyond the scope of this post). SCHB has never made a capital gains distribution, so SCHB is about as tax-efficient as any fund can be.

Investors in a high tax bracket with at least $250,000 may consider direct indexing rather than SCHB, as direct indexing can potentially generate even more tax savings.

SCHB Review: A Recap

The above review of SCHB illustrates that SCHB is a well-constructed, low-cost and tax-efficient index fund that provides diversified exposure to the broad US stock market. SCHB is a great choice in many situations and a tool that I often use personally and professionally.

FAQ’s

Is SCHB a good investment?

Whether SCHB is a good investment or not depends on the definition of “good investment.” If the definition is something that goes up in value, then nobody knows if it is a good investment. If the definition is a well-constructed portfolio that is low-cost and will likely do what it is supposed to do (mirror the US stock market), then yes it is a good investment.

Is SCHB safe long-term?

There is no way to say whether SCHB or any other investment is safe long-term. SCHB owns stocks, which are more volatile than cash or bonds. However, stocks have generated stronger long-term returns than cash or bonds. However, the future may unfold differently than the past, so it is impossible to say whether SCHB is safe in the long-term.

Is SCHB a risky investment?

SCHB owns stocks, which are more volatile than cash or bonds. Some of this risk is diversified away since SCHB owns hundreds of stocks, so there is not too much risk or concentration in any single stock. SCHB is a well-diversified, low-cost index fund, so it is not any more risky than most stock funds.

Is SCHB a buy or sell right now?

Nobody knows the future nor whether SCHB is a buy or sell. SCHB is an index fund and many investors use index funds because they do not believe that investors can consistently time the market or predict the ideal times to buy and sell.

Is SCHB a good ETF to invest in?

The answer to this question depends on each investors’ goals. Investors looking for well-diversified, low-cost, tax-efficient exposure to the US stock market will find a lot to like in SCHB. However, SCHB is not a good ETF to invest in for those looking for something totally different.

Is SCHB good for beginners?

For investors looking for exposure to the US stock market, SCHB is not a bad choice. It can be the core position of a portfolio and provides instant diversification to investors who are building a portfolio.

Does SCHB pay dividends?

Yes, SCHB pays dividends. It is not necessarily a dividend-oriented fund and I would advise investors to focus on total return since dividends reduce a fund’s net asset value. In my view, receiving a dividend is equivalent to selling a small amount of the position. Investors should not focus on SCHB’s dividends or dividend yield.

Which is better SCHB or VTI?

SCHB and VOO are slightly different. Those interested in an in-depth comparison can read my review of SCHB vs VTI.

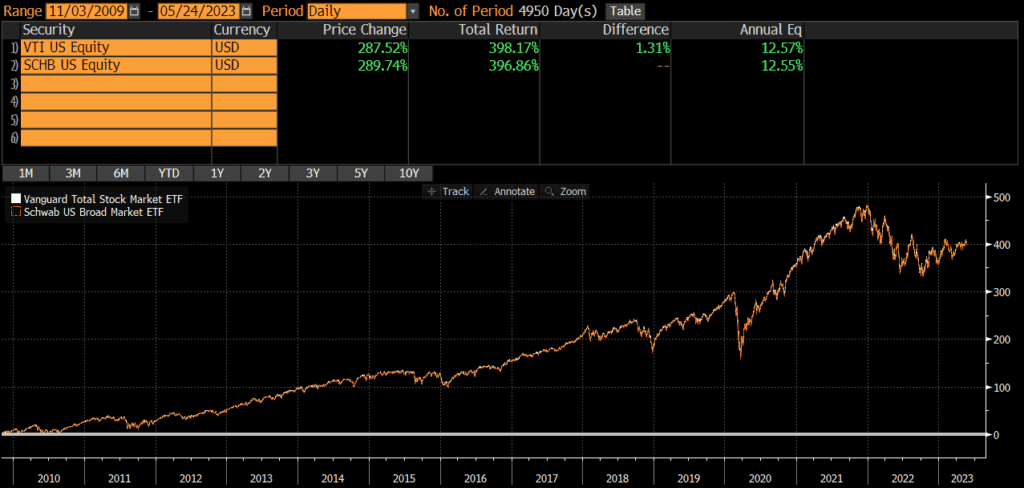

The Schwab US Broad Market ETF (SCHB) and the Vanguard Total Stock Market ETF (VTI) are two of the largest ETFs and are sponsored by Schwab and Vanguard respectively. SCHB and VTI are a core holding of many investor portfolios and many investors compare SCHB vs VTI in order to decide which should be the foundation of their portfolio.

The Short Answer

Although VTI and SCHB track different indices, the risk and return between these two funds is identical and I consider them interchangeable.

VTI was launched in 2001, while SCHB was launched nearly a decade later in 2009. Since then, performance has been identical (as the performance chart below illustrates). The annualized difference in returns is just .02%, which speaks to the similarities in holdings and exposures. The cumulative performance differential over the past two decades is about 1.5%.

Differences between VTI vs SCHB

SCHB tracks the Dow Jones US Broad Market Index, while VTI tracks the CRSP US Total Market Index. However these two indices are basically identical.

Geographic Exposure

Both SCHB and VTI hold essentially 100% US stocks, so I will not dig into country exposures or market classification here. For all intents and purposes, the two funds have identical exposures.

Market Cap Exposure

As the below table shows, the market cap exposure of these two “total market” (meaning they hold large, mid, and small-caps) is identical.

SCHB

VTI

Large-Cap

73%

72%

Mid-Cap

19%

20%

Small-Cap

8%

9%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/24/2023

Sector Weights

The sector weights between SCHB and VTI are nearly identical, which is to be expected given the identical performance.

SCHB

VTI

Basic Materials

2.47%

2.56%

Consumer Cyclical

10.61%

10.39%

Financial Services

12.53%

12.79%

Real Estate

3.14%

3.29%

Communication Services

8.04%

7.61%

Energy

4.40%

4.58%

Industrials

8.98%

9.34%

Technology

26.69%

25.46%

Consumer Defensive

6.49%

6.73%

Healthcare

14.01%

14.44%

Utilities

2.65%

2.80%

Source: ThoughtfulFinance.com, Morningstar; data as of 12/31/2022

Expenses

The expense ratio for both funds is .03%, which extremely low.

Transaction Costs

ETFs are free to trade at many brokers and custodians, so both SCHB and VTI should be free to trade in most cases. Additionally, these funds are among the largest ETFs and are very liquid. The bid-ask spread of both SCHB and VTI is about .01%, so individual investor trades will not generally be large enough to “move” the market.

Tax Efficiency & Capital Gain Distributions

ETFs are typically more tax-efficient than mutual funds, due to their ability to avoid realizing capital gains through like-kind redemptions (a process that is beyond the scope of this post). Neither VTI nor SCHB has never made a capital gains distribution (and I do not expect them to moving forward). Thus, these funds are about as tax-efficient as any fund can be and either fund is appropriate in taxable accounts.

Final Thoughts: VTI vs SCHB

Both SCHB and VTI are large, core funds sponsored and managed by two of the largest investment sponsors in the world. Performance has been extremely similar.

I view these two funds as essentially interchangeable and would not spend any energy splitting hairs to decide which one is “better.” In my opinion, both funds are among the best ETFs out there and investors cannot really go wrong with either.

Growth Equity vs Private Equity: Key Differences and Investment Strategies

Private equity encompasses many types of assets and strategies, including growth equity. Understanding the key differences is important when comparing traditional private equity vs growth equity.

Although a broad asset class, the term “private equity” often refers to “buyout” strategies which involve acquiring controlling stakes in more mature companies, with an emphasis on restructuring and improving operations.

Growth equity typically refers to minority investment stages in younger companies to support expansion initiatives. Like buyout, growth equity investing involves investing in privately-held businesses with established business models and proven revenues.

The level of risk, the industries they target, and their investment approaches vary between growth equity and private equity. By taking a closer look at these key distinctions, investors can make more informed decisions about which strategy suits their goals and risk tolerance.

Growth Equity is a type of Private Equity

Growth equity is sometimes referred to as “growth capital” or “expansion capital” and is an investment strategy typically focused on acquiring minority stakes in late-stage companies that exhibit high growth potential. This infusion of capital aims to fund the companies’ continued expansion plans. Growth equity investors typically include private equity firms, late-stage venture capitalists, and investment funds (such as mutual or hedge funds)1.

While growth equity is a type of private equity, it is distinct from the more common buyout strategy that many people associate with private equity. Buyout strategies typically involve acquiring controlling stakes in mature companies, whereas growth equity investments are targeted at established, growing companies. To further clarify the differences between growth equity and other private equity strategies, consider the following comparison:

Key Differences: Growth Equity vs. Buyout

Growth Equity

Buyout

Minority ownership

Majority or full ownership

Faster growth rate

Slower, more stable growth rates

Less mature companies

More mature companies

Higher risk and return

Lower risk and return

Less focus on leverage

Emphasis on using leverage to enhance returns

Growth equity investments are made in return for equity stakes in the companies and are typically expected to generate significant returns through exponential growth2. Growth equity investments carry a higher degree of risk compared to more traditional private equity buyouts, but they also offer the potential for higher returns as the underlying companies grow and succeed3.

In short, growth equity is a type of private equity that targets established, high-growth companies in need of additional funding to fuel their expansion plans. While it shares some similarities with other private equity strategies, growth equity notably differs from buyouts in terms of ownership, growth rate, company maturity, risk and return, and the focus on leverage. By understanding these key distinctions, one can better appreciate the unique characteristics and potential benefits of growth equity as an investment strategy.

Buyout: In a buyout strategy, investors acquire a controlling stake in an existing company, typically with the goal of improving operational efficiency and financial performance. This can involve restructuring the company, divesting non-core business units, or implementing new management practices.

Growth Equity: Growth equity, which is a type of private equity, focuses on providing capital to fairly established companies with potential for high growth. These investments often take the form of a minority stake, aiming to accelerate the growth of the company by funding expansion initiatives such as entering new markets or making strategic acquisitions.

Risk Profiles

Buyout: Buyout strategies are generally considered to be lower risk due to the fact that buyout has performed well historically, despite notoriously high debt loads. Generally, buyout investors due okay even if the companies do not.

Growth Equity: Growth equity investments are generally considered more risky than buyouts, due to the fact that the companies are less mature. This is despite the fact that growth equity targets companies that are already producing revenues and experiencing growth, even if not yet profitable.

Investment Horizons

Buyout: Investment horizons for buyout strategies are typically longer. This allows for the necessary time to execute operational improvements and exit strategies.

Growth Equity: Growth equity investments, on the other hand, have shorter investment horizons. As their investments aim at accelerating growth, the investors expect to exit when IPO window is receptive and rewarding.

Leverage

Buyout: Leverage is a common component in buyout transactions, with debt often used to finance a significant portion of the acquisition. The use of leverage can amplify returns if the company’s performance improves, but also increases the risk of bankruptcy if the company struggles to service its debt.

Growth Equity: Leverage is less common and less significant in growth equity investments. While debt may still be utilized, the focus remains on equity financing to fuel the company’s growth.

Company Maturity

Buyout: Buyout strategies target more mature companies that often have established revenue streams, a solid market position, and a well-defined business model. The focus is on unlocking value through operational improvements and financial restructuring.

Growth Equity: Growth equity investments are directed towards younger, high-growth companies. These companies may not yet be profitable but are achieving significant revenue growth and demonstrating a scalable business model. The focus is on supporting and accelerating the company’s growth trajectory.

Pros and Cons of Growth Equity

Advantages

Growth equity investments have several advantages for both investors and companies:

Higher Growth Potential: Since growth equity targets late-stage, high-growth companies, there is significant potential for rapid revenue and valuation increases.

Risk and Reward Balance: Compared to venture capital, growth equity investments are less risky due to the proven business models and market positions of the target companies. However, they still offer attractive upside potential compared to traditional private equity buyouts.

Exit Flexibility: Investments in growth-stage companies can lead to various exit options like acquisitions, public offerings, or secondary sales.

Disadvantages

Despite the benefits, there are challenges and potential downsides associated with growth equity investments:

Higher Valuations: High-growth companies can command premium valuations relative to buyouts, which can lead to more expensive investments and lower returns for investors, especially during market downturns.

Competitive Deal Sourcing: Since growth equity investments are targeted by many types of investors, there can be increased competition which drives up prices and risk.

Unpredictable Market Forces: The success of growth equity investments can be influenced by external market factors, such as economic cycles and changes in industry regulations. Such factors can introduce risk and affect a company’s growth trajectory. A volatile stock market may also close the IPO market.

Execution Risk: High-growth companies may face challenges related to scaling their operations, managing working capital, and adapting to new market conditions. Growth equity investors need to be prepared to address these challenges and support their portfolio companies through potential complexities.

Pros and Cons of Buyout

Advantages

Buyout investments, a type of private equity investment, offer several benefits for companies and investors.

Increased efficiency: A buyout can eliminate overlapping services or product offerings, reducing operational expenses and potentially increasing profits. Companies can compare processes and select the most efficient ones.

Access to capital: Buyouts often provide companies with access to substantial capital, allowing them to finance growth initiatives, develop new products, and make strategic acquisitions.

Management expertise: Private equity firms typically have experienced management teams that can help improve the operational performance of a company. This expertise can lead to better decision-making and business strategy execution.

Alignment of interests: Private equity firms usually have a significant ownership stake in their portfolio companies, fostering a close alignment of interests with management. This can lead to better long-term planning and more effective implementation of improvement initiatives.

Disadvantages

Despite the benefits, buyout investments also have some drawbacks that should be considered.

High leverage: Buyouts often involve substantial amounts of debt, which can increase the financial risk for companies. High leverage can lead to higher interest expenses, making it more challenging for a company to achieve its financial objectives.

Control & influence: Following a buyout, the private equity firm may exert significant control over the company’s operations and decision-making. This influence can lead to disagreements between the private equity firm and the current management team.

Short-term focus: Some buyout investments may have a relatively short time horizon. A short-term focus can sometimes result in decisions being made with an eye towards exiting the investment quickly, rather than long-term value creation.

Fees: Private equity firms charge management fees and carry interest, which can reduce the overall return for investors. These fees can be substantial, and it is essential to weigh them against the potential returns when considering buyout investments.

Private Equity vs Growth Equity: What To Invest In?

To choose the right investment strategy, investors should also examine how each type of investment aligns with their objectives. Growth equity and private equity investments each present unique opportunities and risks. For example:

Growth equity investments can offer higher potential returns due to the faster growth rate of the target companies. However, they also come with a higher level of risk, as these companies may not yet be profitable and may require additional capital to continue their growth trajectory.

Private equity investments often target companies with a proven track record of profitability, which can provide more stable returns. However, the potential for significant capital appreciation may be limited as these companies are typically more mature and have slower growth rates.

In summary, the right investment strategy will depend on an investor’s risk tolerance, return expectations, and overall investment objectives. By carefully evaluating the differences between growth equity and private equity, and considering the factors mentioned above, investors can make informed decisions that align with their goals.

MOIC is a common metric in performance reporting for private equity, venture capital, real estate, and other private investments. It is a valuable tool, but it is insufficient in and of itself. It is important to understand how the MOIC figure is generated as well as look at other return metrics such as IRR, TVPI, CoC, and so on.

MOIC Definition

MOIC stands for Multiple On Invested Capital. It expressed return as a multiple of invested capital. Invested capital typically refers to the amount of money that is actually invested (by a fund, typically), so MOIC is often used to measure the performance of private investments. MOIC can be quoted on a gross or net of fees basis.

MOIC Formula

MOIC Example

Let’s assume an investor purchases a building for $10 million. Over the next few years, the investor receives $2 million of distributions and the building appreciates in value to $13 million. In this case, the total realized value is $2 million and the total unrealized value is $13 million. The total cost was $10 million. So the MOIC would be 1.5x.

MOIC Calculation

In the above example, we get 1.5x by adding $2 million and $13 million and then dividing by $10 million.

Shortfalls of MOIC

MOIC is an immensely useful metric for evaluating private equity investments. However, MOIC does have some limitations as well.

MOIC Does Not Consider Time

The first major problem with MOIC is that it does not consider time. We do not know whether an investment with a 2x MOIC is good or bad. It the investment was 2 years ago, the 2x MOIC is great performance. If the investment was made 15 years ago, the 2x MOIC looks rather low.

MOIC Does Not Consider Time Value of Money

Even if two private equity funds are identical in terms of total MOIC and time invested, there can be major differences in return. Consider two different five-year funds, Fund A and Fund B. Both funds have generated a 1.6x MOIC on their investments. Yet, this is insufficient to know which fund performed better.

Lets assume Fund A called 100% of capital immediately. After two years, it returned 130% of that amount back to investors and an additional 30% at the end of the five year period. This is a 1.6x net MOIC.

Alternatively, consider Fund B which also called 100% of capital immediately. It made no distributions for five years and then returned 160% of capital back to investors. This is also a 1.6x net MOIC.

Even though the two funds have generated the same MOIC from their investments, Fund A clearly performed better than Fund B. Investors could have taken the initial distribution from Fund A and reinvested it for the remaining years, whereas investors in Fund B had a total return of 1.6x.

While MOIC is important, time matters and the time value of money matters. This is why investors should never only look at MOIC. They should also look at IRR and/or understand the timing of the cashflows that generated the MOIC figure. Read my summary on MOIC vs IRR.

MOIC May Not Represent Investor Returns

The IC in MOIC stands for invested capital, which technically means capital that the fund invested. But MOIC is often calculated at the asset level and reported gross of fees. Investors may want to compare MOIC to TVPI to get a better read on investor returns.

Impact of Recycling on MOIC

A private equity fund will commonly be receiving distributions from the assets that it owns at the same time that it is calling capital from investors. Consider a $100 million fund that receives a $5 million distribution and simultaneously needs to make a $5 million investment. A popular tactic is to use the proceeds to fund the capital call (rather than distributing the $5 million and then issuing a capital call for them to send it back). In this case, the Multiple (numerator) is increasing and the Invested Capital (denominator) is increasing, but the investor has not contributed any more cash. So the Cash-on-Cash (CoC) return is higher than what the MOIC indicates. Many funds market their “Max Out Of Pocket” exposure, which is another way of saying what percent of an investor’s commitment they end up actually contributing (once recycling is accounted for).

Recallable Distributions (and other shenanigans)

Some private equity funds may distribute capital back to investors very early and classify it as a recallable distribution, meaning that it can be called again. The impact on MOIC is that it reduces the denominator, so MOIC numbers increase. Funds may also make distributions early on (even if they are going to recall it again) because it can permanently increase the IRR metrics. I’m not a huge fan of these recallable distributions, but they are out there and it is important to understand how they can impact MOIC and other performance metrics. The main point here is that fund can play (what I consider) games by re-classifying cash flows.

Investing can be a powerful tool for wealth creation and financial security, but it is not without its pitfalls. The journey to becoming a successful investor is often marked by learning from past mistakes and adjusting strategies accordingly. Below are some common investing mistakes that I’ve seen and I hope readers who are new to the world of investing avoid these potential mistakes.

Some investors jump into the market without first educating themselves on the basics of investing. Others may be swayed by emotions or swamped under the influence of their cognitive biases. It is important for investors to understand these common errors and implement strategies to mitigate them.

Investing without a plan

One common investing mistake that I see is beginning to invest without a clear plan. Some people start purchasing a few stocks or funds based on the recommendations of friends, family, or media sources. However, without a concrete strategy, they may struggle to manage their investments effectively.

A well-thought-out investment plan outlines an investor’s financial goals, risk tolerance, and time horizon. It helps them choose appropriate investments that align with their objectives and comfort level. A plan serves as a framework, helping investors to understand each decision within the larger context.

Having an investment plan and reviewing it periodically can help investors stay on track and make necessary adjustments as their circumstances change. This proactive approach enables them to manage their wealth in a controlled manner, without being swayed by market fluctuations or emotional decisions.

Insufficient Diversification

Another very common investing mistake is insufficient diversification. This occurs when an investor’s portfolio is heavily concentrated in a single asset class or sector. Diversification is crucial because it helps reduce the overall risk associated with a portfolio by spreading investments across a range of asset classes and sectors.

For example, if an investor’s portfolio comprises primarily technology stocks, they may be exposed to significant risk if the technology sector experiences a downturn (read my review of VTI vs QQQ for a very simple example of this). To mitigate such risks, it’s advisable for investors to diversify their holdings with a mix of stocks, bonds, and other investment vehicles.

Below are just a few dimensions of diversification, but there are many more:

Asset allocation: This involves allocating a portfolio among various asset classes like equities, bonds, and cash equivalents. By maintaining a balanced portfolio, investors can lessen the impact of a poor-performing asset class on their overall returns.

Geographic diversification: Investing in multiple countries and regions can provide an additional layer of protection. Different economies may perform differently at various times, shielding investors from the negative impact of a single market downturn.

Sector diversification: This practice entails diversifying among different industries or sectors, such as financial services, healthcare, or consumer goods. Different sectors may have distinct performance patterns, and a well-diversified portfolio can benefit from the positive performance of various industries.

Investment style diversification: Some investors may benefit from diversifying across various investment styles, like growth, value, or dividend investing. This can offer exposure to companies with diverse characteristics and minimize the impact of poor performance in a particular investment style.

By employing sufficient diversification, investors can reduce volatility, weather market fluctuations more effectively, and better protect their capital against adverse events.

Ignoring Costs and Fees

Unfortunately, ignoring the costs and fees associated with various investment vehicles is too common. Expenses can significantly impact an investor’s overall returns in the long run, particularly in situations where the fees are ongoing or compound over time.

Many funds have an expense ratio, which are annual expenses paid by investors (expressed as a percentage of their assets). These fees can vary widely, with some index funds charging 0%, while some actively managed funds can charge upwards of 1%-2% (or more). Over time, these seemingly small percentages can make a substantial difference in an investor’s portfolio.

When it comes to trading individual stocks, investors should also be mindful of transaction fees. Many brokerage firms offer low-cost or commission-free trades, but some may still charge per-trade fees, especially for options or ADRs. Ignoring these fees can add up in cases when investors are actively trading in and out of positions.

By paying close attention to costs and fees, an investor can make informed decisions that take into account the potential impact on their overall returns. This awareness will help them avoid the trap of ignoring these essential aspects of investing and avoiding these common investing mistakes.

Emotional Investing

As humans, many investors tend to make decisions based on their emotions rather than focusing on objective financial analysis. They might buy or sell assets due to fear, greed, or other strong feelings rather than considering the underlying fundamentals of the investment.

An investor’s emotions often take the front seat during market fluctuations. For instance, they might be tempted to sell a position during a brief market downturn. This panic selling can lead to poor investment results, as many investors sell at a lower price and purchase at a higher price which is not a logical approach.

Sometimes investors become overly attached to a particular company or security. Perhaps they have an emotional connection or loyalty to the brand that clouds their rational judgment. This bias can lead them to hold onto the investment for too long, even when its value declines or it’s no longer strategically relevant within their portfolio.

It is essential for investors to be aware of their emotions and develop strategies or accountability to keep them in check. By doing so, they can improve their overall investment decision-making process and be less susceptible to common investing mistakes.

Chasing Past Performance

One common investing mistake is chasing past performance. Investors often examine the historical returns of a stock or fund and assume that it will continue to perform similarly in the future. However, past performance is not necessarily indicative of future results.

There are several reasons investors should not rely solely on past performance when making investment decisions. First, the market is constantly changing, and factors that may have contributed to a specific stock or fund’s success in the past may no longer be relevant.

Timing the Market

A related investing mistake is attempting to time the market. This occurs when investors try to predict when the market will rise or fall, buying or selling investments based on these predictions. The belief is that by doing so, they can maximize gains and minimize losses.

However, timing the market can be challenging even for seasoned professionals, as it relies on accurately forecasting market movements. Many factors, such as economic indicators, political events, and global issues, can impact the market unpredictably.

Another problem with market timing is the psychological impact it can have on investors. As market fluctuations create uncertainty, investors may experience emotional distress leading to impulsive decision-making. Fickle behaviors, such as panic selling during a market downturn or exuberant buying during a market upswing, can harm an investor’s long-term financial goals.

Instead of trying to time the market, it is often more beneficial to adopt a strategy of consistent, long-term investing. This approach involves regularly investing, regardless of market conditions, and focusing on growing investments over time. By doing so, investors can take advantage of compounding returns and reduce the risk associated with market timing.

In recent years, the debate between renting and owning a home has become increasingly relevant, as both rents and home prices continue to climb. Some tend to believe that buying a house is the best route to financial stability and security. However, there are numerous advantages to renting a home and should be considered when deciding between the two options.

Renting provides flexibility which allows individuals to move with greater ease and less long-term commitment than homeownership. Renting also eliminates MANY costs, both expected and unexpected. For many, it is clear that renting offers a more convenient and financially-sound solution.

There are even many financial experts who advocate for renting. James Choi was recently on the Planet Money podcast discussing why he’s renter for life and personal finance guru (and now Netflix star) Ramit Sethi also rents. There does seem to be a bias towards owning in the US, but renting is a better alternative for many people.

Financial Benefits of Renting (vs Buying)

When it comes to deciding between renting and buying a home, there are several financial advantages to renting.

No Maintenance Costs

One of the main advantages of renting is that tenants are not responsible for maintenance costs. When something breaks or needs repair in a rental property, it is typically the landlord’s responsibility to fix it. This can save renters a significant amount of money, as homeowners are faced with ongoing expenses for repairs and upkeep. Renters don’t have to pay $1,000 when the water heater needs replacement or $15,000 for a new roof, or $3,000 to find and fix an unknown plumbing issue. These expenses add up quickly and are not always taken into account by prospective homebuyers.

No Property Taxes

Renters do not have to pay property taxes. Homeowners, on the other hand, are subject to property taxes which can be quite substantial, especially in states or cities with high property values and/or property tax rates.

No Homeowners Insurance

Renters do not need to purchase homeowners insurance, which can be a considerable expense for homeowners. While renters should still have renters insurance to cover their personal belongings and liability, this is typically less expensive than homeowners insurance.

Lower Upfront Costs

Renting also tends to have lower upfront costs compared to buying a home. Rather than coming up with a large down payment to secure a mortgage, renters usually only need to provide a security deposit and first month’s rent. This can be a more affordable option for those who may not have a significant amount of savings. Even those who have saved a lot might be better off investing that capital rather than using it as a down payment.

Rent Control

In some cities, there are rent control laws that limit how much a landlord can increase rent each year. This can offer stability to renters, as their monthly expenses are predictable and may be protected from inflation and market fluctuations.

Savings on Amenities

Some rental properties include amenities like a gym, pool, or utilities as part of the rent. When these services are included, it can save renters money compared to homeowners who may have to pay separately for these amenities. In addition, renters can benefit from shared common areas and services provided by the landlord.

Renting can be a wise financial decision for many people, depending on their financial situation and lifestyle preferences. By considering the factors listed above, potential renters can make a more informed choice about whether renting or buying is the best option for them.

Renting is not necessarily throwing money away

Many people believe that renting a property is akin to throwing money away. However, this is not always the case. There are several valid reasons why renting can be a smarter financial decision in certain situations.

People often say this because rent goes to a landlord rather than paying down equity. Yet, in the early years of a mortgage, barely anything goes towards principal and most of a mortgage payment goes towards interest. Paying a high interest rate can be more akin to throwing money away than renting in many cases.

It is important to take into account the numbers. From a financial perspective, the decision of whether to rent or buy depends largely on the current housing market in a specific area. According to an analysis by Realtor.com, renting is cheaper in 45 out of the 50 largest U.S. cities.

Buying a home may be the ultimate goal for some people, but renting should not be seen as a waste of money. For many, it can be a smarter and more financially viable option in the short term, providing flexibility, lower expenses, and the ability to invest money elsewhere.

Flexibility in Lifestyle and Location

Easier to Relocate

One of the significant advantages of renting over homeownership is the ease of relocation. Renters enjoy the freedom to move for various reasons, including new job opportunities or to experience different neighborhoods within or outside their cities.

For many young people and millennials, this flexibility is crucial because they may not have settled into a permanent career or location. In metropolitan areas, renting an apartment or a house is often more accessible, allowing residents to experience the unique benefits of city living. Renting provides the opportunity to explore different communities and neighborhoods, gauging their accessibility, proximity to schools, and overall cultural compatibility.

Adapting to Life Changes

Renting also allows individuals and families the ability to adapt to life changes with considerably less commitment than homeownership. When renting, people have the option to upsize or downsize accommodations according to their needs. For example, if a family grows or an individual’s living situation changes, renting can accommodate these fluctuations without the large financial commitment of buying a home.

Moreover, apartment living often features greater access to community amenities, such as gyms, pools, and recreational areas, without added costs for maintenance. This added convenience can suit various lifestyles, especially for those who prioritize leisure and ease of living over long-term financial investments.

Renting offers significant benefits for those who value flexibility, adaptability, and a diverse lifestyle experience. As individuals and families navigate an ever-changing world, the ease of relocation and a focus on the present moment may supersede long-term commitments like buying a home.

Reduced Maintenance and Repair Responsibilities

In my view, one of the main advantages of renting a property instead of owning one is the reduced responsibility for maintenance and repairs. When living in a rented apartment or house, it’s the landlord’s duty to deal with any maintenance issues that may arise, such as fixing a leaky faucet, replacing a broken appliance, or addressing structural problems. This can save renters both time, money and stress, as they won’t have to worry about handling these tasks themselves or paying for the services of a professional. This peace of mind is worth a lot in many cases.

Investment Alternatives to Homeownership

Diversifying Your Portfolio

One of the benefits of renting over buying a home is the opportunity to diversify your investment portfolio. Homeownership is often considered a long-term investment, but it is not diversified at all and many markets can lose value. By choosing to rent instead of own, individuals can allocate the capital that would have gone towards a mortgage to a variety of investment options. This includes stocks, bonds, and even alternative investments.

By spreading investments across various asset classes, individuals are less likely to experience significant losses if the real estate market suffers a downturn. Compare this to a homeowner who may face declining property values or be stuck with a mortgage that exceeds their home’s value.

Lower Barriers to Entry

Another advantage to renting over buying is the lower initial costs associated with entering the rental market. Homeownership often requires a large down payment, as well as additional costs such as closing fees, inspection costs, and property taxes. Renters typically face lower upfront costs, which include security deposits and moving-related expenses.

In addition, renters often have better access to high-demand locations, such as city centers and popular neighborhoods, where property prices and mortgage interest rates may be prohibitive for potential homeowners. By avoiding the substantial costs of homeownership, renters can redirect funds towards different lifestyle expenses or investment opportunities.

Risks of Homeownership

Unexpected Costs

One risk of homeownership is the potential for unexpected costs. When owning a home, there are numerous expenses that can arise unexpectedly, such as maintenance and repair costs. For example, if the HVAC system needs to be replaced or a roof needs repairing, these costs can be substantial and must be covered by the homeowner.

Real Estate Market Risk

Another risk factor of homeownership is the real estate market risk. The housing market can be volatile, and homeowners need to consider fluctuations in home values when making long-term financial plans. A perfect example is the 2008 housing market crash, where numerous homeowners saw the value of their homes decrease significantly.

Renters, on the other hand, typically experience less exposure to the fluctuations of the housing market. They can more easily adapt to changing economic conditions, which can be especially beneficial for younger renters and millennials who may move to different cities or communities for job opportunities or to be closer to better schools.

There are various risks associated with homeownership that can make renting a more attractive option for many individuals. With the potential for unexpected costs and the uncertainty of the housing market, renters can enjoy a greater sense of flexibility and financial stability as they navigate their personal and professional lives. The “American Dream” of homeownership may not be the best choice for everyone, especially in a rapidly changing society and economy.

Final Thoughts: is it better to rent or buy?

Taking all these factors into account, it becomes apparent that renting can offer several benefits that make it an attractive alternative to owning a home. By considering personal preferences, financial capabilities, and geographic location, individuals can make an informed decision that best suits their needs and desires.

While many people tend to focus on the dollars and cents and financial projections, the flexibility that comes with renting cannot be overstated. Renters have the ability to change their living arrangements more easily if life circumstances or job opportunities change. This adaptability can be essential for those who value mobility or do not want the long-term commitment that homeownership entails.

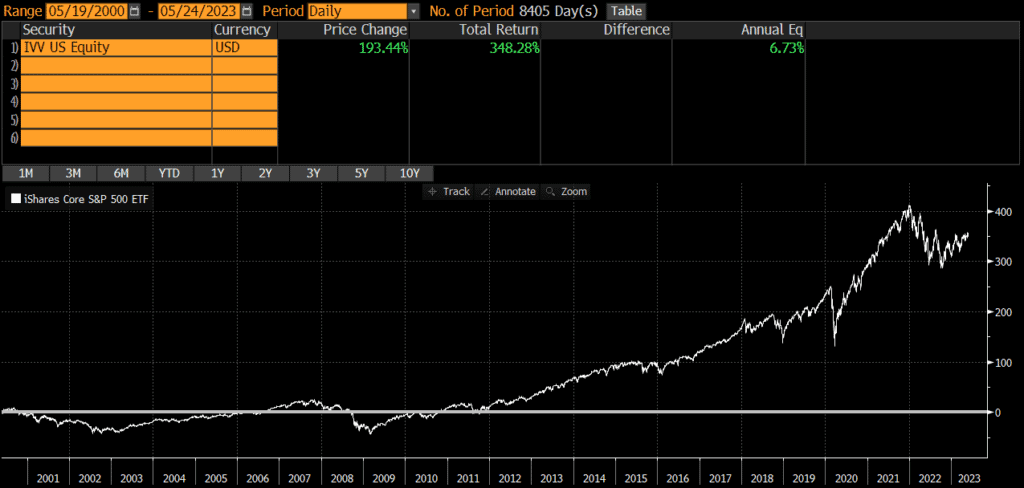

The iShares S&P 500 ETF (symbol: IVV) is one of the largest exchange-traded funds (ETFs) in the market and widely used by both individual and institutional investors. IVV is a low-cost index fund, which tracks the S&P 500 Index. The fund seeks to provide exposure to the US stock market at a very low price. The fund is the core of many portfolios and the below review of IVV will evaluate why that is.

The first thing most investors want to know about is performance, so we will start there. According to Bloomberg, since the fund’s inception 23 years ago, IVV has returned nearly 7% per year. Of course, this figure can go up or down and the returns in any single year are unlikely to be 7%. From 2001 through 2022 (22 years), IVV was up in 17 years and down in 5 years. The average return in the up years was 16.7%, while the average return in the down years was -18.6%.

Source: ThoughtfulFinance.com, Bloomberg

IVV Risks

IVV owns stocks which are more volatile than cash or bonds. While the returns are higher than cash or bonds, investors need to be prepared to stomach volatility and be able to hold for the longer-term. IVV was down nearly 35% during the covid pandemic and down over 25% at one point in 2022. It was also down nearly 50% in the 2000-2003 recession and declined over 55% during the 2007-2009 recession. This is not necessarily worse than other similar funds, but it is a characteristic of stocks that investors need to be aware of.

IVV Portfolio

Fund performance is ultimately driven by a fund’s holdings and exposures, so our IVV review will examine these items.

IVV Holdings

IVV (and its underlying index) is incredibly diversified, holding over 500 stocks. This represents the large-cap segment of the US stock market.

IVV

S&P 500

Number of Stocks

503

503

Sources: ThoughtfulFinance.com, iShares (as of 4/30/2023)

IVV Country Exposures

IVV only owns US-based companies. Investors looking for international exposure may pair IVV with international ETFs or simply hold a global ETF.

IVV Market Cap Exposure

IVV is primarily a large-cap fund which seeks to represent the largest US stocks. Even though the fund holds some mid-caps, performance is primarily driven by the large-cap exposure.

IVV

Large-Cap

83%

Mid-Cap

17%

Small-Cap

0%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/22/2023

IVV Sector Exposures

IVV is extremely diversified across sectors and mirrors the approximate weights of the broad US stock market.

IVV

Basic Materials

2.27%

Consumer Cyclical

10.35%

Financial Services

12.34%

Real Estate

2.53%

Communication Services

8.75%

Energy

4.32%

Industrials

8.13%

Technology

27.42%

Consumer Defensive

7.02%

Healthcare

14.14%

Utilities

2.73%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/22/2023

Expenses

No review of IVV would be complete without an in-depth look at the explicit and implicit costs of trading and holding IVV.

IVV Expense Ratio

IVV’s expense ratio of .03% is among the lowest of any large-cap funds. Even if another fund is free, three basis points is not a material difference in my opinion.

IVV Transaction Costs

ETFs are free to trade at many brokers and custodians, so IVV should be free to trade in most cases. Additionally, it is among the largest ETFs and is very liquid. The bid-ask spread of IVV is about .01%, so individual investor trades will not generally be large enough to impact or move the market.

IVV Tax Efficiency

Like most index funds, IVV is very tax-efficient. Unlike actively-managed funds, passively-managed index funds typically have less trading and lower turnover. This results in fewer taxable events and higher tax efficiency.

ETFs are typically more tax-efficient than mutual funds, due to their ability to avoid realizing capital gains through like-kind redemptions (a process that is beyond the scope of this post). IVV has never made a capital gains distribution, so IVV is about as tax-efficient as any fund can be.

Investors in a high tax bracket with at least $250,000 may consider direct indexing rather than IVV, as direct indexing can potentially generate even more tax savings.

IVV Review: A Recap

The above review of IVV illustrates that IVV is a well-constructed, low-cost and tax-efficient index fund that provides diversified exposure to the US stock market. IVV is a great choice in many situations and a tool that I often use personally and professionally.

FAQs

Is IVV a good investment?

Whether IVV is a good investment or not depends on the definition of “good investment.” If the definition is something that goes up in value, then nobody knows if it is a good investment. If the definition is a well-constructed portfolio that is low-cost and will likely do what it is supposed to do (mirror the US stock market), then yes it is a good investment.

Is IVV safe long-term?

There is no way to say whether IVV or any other investment is safe long-term. IVV owns stocks, which are more volatile than cash or bonds. However, stocks have generated stronger long-term returns than cash or bonds. However, the future may unfold differently than the past, so it is impossible to say whether IVV is safe in the long-term.

Is IVV a risky investment?

IVV owns stocks, which are more volatile than cash or bonds. Some of this risk is diversified away since IVV owns hundreds of stocks, so there is not too much risk or concentration in any single stock. IVV is a well-diversified, low-cost index fund, so it is not any more risky than most stock funds.

Is IVV a buy or sell right now?

Nobody knows the future nor whether IVV is a buy or sell. IVV is an index fund and many investors use index funds because they do not believe that investors can consistently time the market or predict the ideal times to buy and sell.

Is IVV a good ETF to invest in?

The answer to this question depends on each investors’ goals. Investors looking for well-diversified, low-cost, tax-efficient exposure to the US stock market will find a lot to like in IVV. However, IVV is not a good ETF to invest in for those looking for something totally different.

Is IVV good for beginners?

For investors looking for exposure to the US stock market, IVV is not a bad choice. It can be the core position of a portfolio and provides instant diversification to investors who are building a portfolio.

Does IVV pay dividends?

Yes, IVV pays dividends. It is not necessarily a dividend-oriented fund and I would advise investors to focus on total return since dividends reduce a fund’s net asset value. In my view, receiving a dividend is equivalent to selling a small amount of the position. Investors should not focus on IVV’s dividends or dividend yield.

Which is better IVV or VTI?

IVV and VTI are slightly different. Those interested in an in-depth comparison can read my review of VTI vs IVV.

Deciding between renting and buying a home in California can be a challenging task. While the state is known for its stunning coastline, abundant opportunities, and sunny weather, the high costs associated with living in California often leave people wondering if it’s better to rent or own their homes.

The average rent in California tends to be significantly higher than the national average, with prices varying greatly depending on location, property type, and amenities. Meanwhile, buying properties in the state can be a considerable investment, due to the substantially higher home values when compared to other states. Ultimately the decision to rent or buy in California depends on an individual’s financial situation, lifestyle preferences, and future plans.

Balancing these factors requires a careful evaluation of one’s circumstances. Utilizing resources such as Rent vs Buy Calculators can also be a valuable tool to help individuals make a well-informed decision based on their unique situation. (This tool takes into account various factors like everyday costs of renting, renter’s insurance, security deposit for renting, and expenses related to owning a home. It can help you get an idea of the financial aspects involved in both renting and buying properties, allowing you to make a more informed decision based on your individual circumstances.)

Financial Considerations

Cost of Living in California

California is known for its high cost of living, which impacts both renters and homeowners alike. For those already in California (or those committed to living in California), the cost of buying should always be compared against the cost of renting. For instance, someone might think a $5,000/month mortgage is a lot. But if the alternative is to rent for $4,000, then they should re-frame the question from a $5,000 absolute cost to a $1,000 difference. A slight change in thinking, but it takes into account the alternative costs.

Non-Californians who are considering a move to California should consider the cost of living. It is essential for anyone considering a move to California to research these factors and evaluate them alongside their personal income to determine how feasible it is to live in California.

Housing Prices and Rent Rates

California has some of the highest housing prices and rent rates in the nation. On the other hand, rent rates also tend to be considerably higher than the national average, which may help offset some of the costs associated with buying a home for some individuals.

Down Payments

When considering purchasing a home in California, one must also factor in the closing costs and down payments. For first-time homebuyers, the down payment on a conventional loan can be as low as 3%. Seasoned homebuyers may need a down payment of at least 5%. FHA loans often require a 3.5% down payment, while USDA and VA loans may not require any down payment. Many homebuyers using qualified mortgage (QM) loans put 20% down, while non-QM loans typically require a down payment of 10% to 30%.

Closing Costs, Unexpected Expenses, etc.

When it comes to determining whether renting or buying is the right choice, it depends on the numbers. Renting versus buying ultimately comes down to the math – comparing not only mortgage payments and rent rates but also property taxes and other expenses. The decision is highly dependent on an individual’s personal financial situation, preferences, and long-term goals. It is always recommended that potential homeowners and renters run their own numbers or seek professional assistance to accurately assess their options.

Additional Costs and Expenses of Homeownership

When considering whether to rent or buy a home in California, it’s essential to take into account the various additional costs and expenses associated with homeownership. This section will outline several of these cost factors, covering Mortgage Insurance and Taxes, Maintenance, Utilities, and Upkeep. Renters typically save A LOT of money by not being responsible for maintenance and repairs (although they also miss out on the potential for appreciation).

Mortgage Insurance

Homebuyers who make a down payment of less than 20% are typically required to pay for private mortgage insurance (PMI). This additional cost should be factored into the monthly mortgage payment.

Hazard Insurance

Hazard insurance protects against fires, floods, etc. The annual cost often runs between $1,000-$2,000 for median priced homes in California, although the costs are rising due to the recent spate of natural disasters and fires.

Property Taxes

Property taxes are an essential expense to consider as a homeowner. In California, these taxes are often around 1.25% of the property value per year. California also has a law referred to as Prop 13, which limits property tax increases to 2% per year. This obviously keeps property taxes predictable and keeps a lid on expenses, although it is also blamed for the sky high property prices and low for sale inventory in the state. Lastly, I should note that there is a risk of Prop 13 being rolled back. I do not expect this to happen, but its been floated as an idea before and similar propositions have come up for a vote.

Maintenance

Owning a home also comes with responsibility for maintaining and repairing the property. Maintenance costs can range from regular upkeep, such as landscaping and painting, to larger expenses like roof replacements or plumbing repairs. It’s crucial for prospective homebuyers to establish a budget for repairs and unexpected expenses to ensure they can afford to maintain their investment in the long run.

Utilities

Utilities are an essential expense for any living situation. For homeowners, utilities may include electricity, gas, water, sewer, and trash services. While renters often have some or all of these costs included in their monthly rent, homeowners must budget for all utility expenses on top of their mortgage payments and other costs.

To determine if renting or buying in California is the right option, it’s essential to carefully weigh these additional costs and expenses. The answer will always depend on the individual’s financial situation and long-term goals, as well as the specific numbers involved. By taking the time to evaluate all aspects thoroughly, prospective homebuyers can make an informed decision about their housing future.

Pros and Cons of Renting and Buying in California

Pros of Renting

Renting a home in California has its advantages, primarily flexibility and fewer responsibilities. One benefit of renting is that tenants can easily relocate without the time-consuming and costly process of selling or buying properties or arranging for renters. And while the average rent in California is much higher than the national average, is still cheaper than many peoples’ mortgage payments.

Another advantage is the freedom from maintenance costs, as the landlord is responsible for most property repairs. For renters, this means lower expenses and fewer responsibilities than homeowners. Furthermore, cities with strict rent control and tenant-friendly laws make renting even more appealing for long-term residents.

Pros of Buying

While renting has its merits, there are also benefits of homeownership in California. Historically, a primary benefit has been equity appreciation. Homeowners who secure a mortgage are able to essentially fix their housing costs for 30 years (or however long their mortgage is). A portion of monthly payments are credited toward principal, which builds equity in a property. Of course, any upside appreciation is captured by the homeowner.

When owning a property, individuals also have the freedom to make alterations or improvements to the space without the need for landlord permission. Moreover, some tax advantages come with homeownership, including the possibility of deducting mortgage interest and property taxes from income taxes.

Cons of Renting

Despite the flexibility offered by renting, tenants also face some drawbacks. Renters are continuously subjected to landlord approvals, meaning simple tasks like changing a room’s color or adopting a pet may become complicated bureaucratic endeavors. Dealing with another party regarding one’s home is rarely fun.

Cons of Buying

Homeownership in California comes with its financial challenges, such as the often-prohibitive initial costs of buying a property. Buyers must also budget for ongoing expenses like property taxes, insurance, and maintenance costs, which can add up quickly.

Without potential equity appreciation, renting is probably the better financial choice for many. Many people buy because they expect inflation to push rents and prices up in the future. However, is we relax this assumption, then buying is not as attractive in the long-term.

Overall, the decision of renting versus buying in California depends on various factors, including financial and non-financial considerations. Prospective residents must carefully weigh their options and thoroughly evaluate their personal situation to make the best choice for their unique circumstances.

Housing and Real Estate Market Trends

Housing Market Overview

California’s housing market has long been known for its high prices and demand. The state has experienced significant growth in recent years, with the median home price increasing in recent years. While some areas have seen more substantial price increases, there are notable variations city to city. In high-cost areas like San Jose, San Francisco, and Los Angeles, the gap between renting and buying has been larger than in other regions.

Recent Changes Due to the Pandemic

The COVID-19 pandemic had a considerable impact on the California housing market. Some trends observed during this time include:

A shift in buyer preferences: Homebuyers have been looking for more space and amenities, leading to higher demand for suburban properties. This has contributed to price increases in more affordable, outlying suburbs and smaller metro areas.

A drop in the number of homes sold: The California housing market saw a 37.5% decrease in the number of homes sold in September 2022 compared to the previous year. The decline in inventory has pushed prices even higher.

The pandemic drove for sale inventory to historically low levels.

These changes have made the decision to rent or buy in California much more complex, although they probably tilt the scales more towards renting. Every city and neighborhood is different, so it’s essential for potential buyers and renters to work closely with a knowledgeable real estate agent who can provide guidance and assistance in evaluating their options based on the latest trends and data.

Long-term Financial Implications

Home Ownership and Equity Growth

When considering buying a home in California, one of the key aspects to examine is the potential for equity growth. Historically, home prices in the US have risen, allowing homeowners to build equity over time. In California, the housing market has followed a similar trend, with home prices increasing in many regions.

However, it is essential to remember that past trends may not always predict the future. Several factors, such as the local economy, job market, supply and demand, and lender policies, can influence home prices. Consequently, it is crucial to analyze your specific situation and the housing market in your desired location before deciding to buy.

Investments and Stock Market

Another long-term financial factor to consider when deciding between renting or buying in California is the potential return on investment (ROI) from other financial opportunities, such as stock, real estate investments, and so on. In some cases, investing in stocks or other financial assets can result in a higher ROI than purchasing a home.

To determine which option is more favorable, compare the possible returns from investing in the stock market to the potential equity growth in your desired property. It is important to evaluate the risk, potential reward, and liquidity of these investments.

When it comes to deciding whether to rent or buy in California, the answer often depends on the numbers. Carefully analyzing the potential equity growth of a property, comparing ROI of alternative investments, and considering your personal financial situation can help inform your decision. Keep in mind that the future may not always mirror the past, so it is crucial to be cautious and consider various scenarios.

Personal Factors to Consider

When deciding whether to rent or buy in California, it’s okay to take non-financial personal factors into account too!

Career and Job Stability

One of the most important aspects to consider is your career and job stability. Moving frequently for work can impact your choice between renting and buying. If your career requires you to relocate often or you anticipate changing jobs in the near future, renting may be a more suitable option for you.

It’s crucial to remember that buying a home involves upfront costs like down payments, closing costs, and moving expenses. Renting provides more flexibility, as you can easily move without worrying about selling a property or breaking a mortgage.

Financial Goals

Another critical factor to consider is your financial goals. Before deciding on renting or buying, you should assess your current savings, debt level, and future financial plans. Buying a home in California may require a larger down payment and higher monthly mortgage payments, which might conflict with other financial goals or require careful budgeting. Consider whether your financial goals align with the costs and benefits of renting versus buying, as well as your ability to manage the ongoing expenses associated with homeownership.

Lifestyle Preferences

Lastly, think about your lifestyle preferences and how they relate to your living situation. Owning a home provides more autonomy in terms of decorating, renovating, and customizing your living space. Homeownership can also offer a sense of stability and permanence. This can be especially important if you have school-age children and staying at the same school or within the same district is important.

On the other hand, renting may be better suited for those who prefer flexibility, minimal responsibility for property maintenance, and the ability to change apartments or neighborhoods more easily. You should also consider proximity to schools, work, and recreational activities that are important to you.

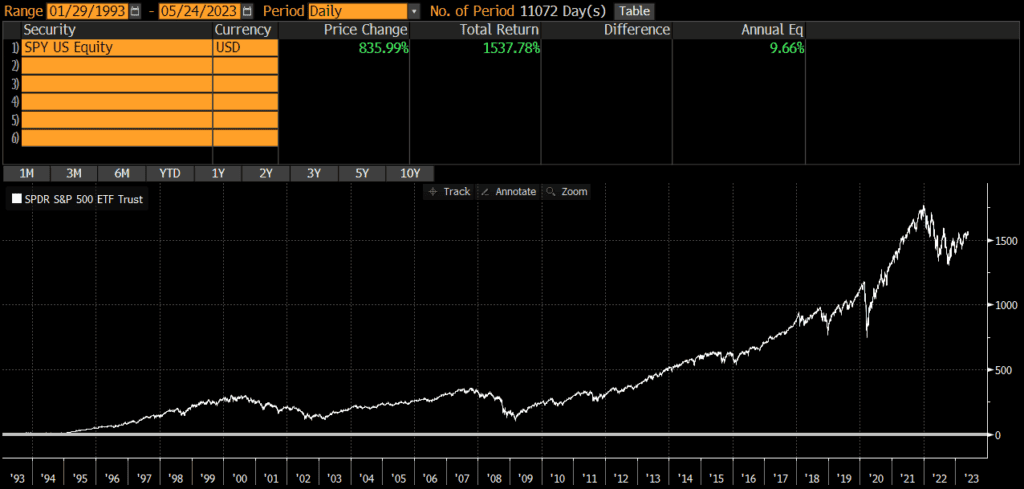

The State Street SPDR S&P 500 ETF Trust (symbol: SPY) is the oldest and one of the largest exchange-traded funds (ETFs) in the market and widely used by both individual and institutional investors. SPY is a low-cost index fund, which tracks the S&P 500 Index. The fund seeks to provide exposure to the US stock market at a very low price. The fund is the core of many portfolios and the below review of SPY will evaluate why that is.

The first thing most investors want to know about is performance, so we will start there. According to Bloomberg, since the fund’s inception 30 years ago, SPY has returned nearly 10% per year. Of course, this figure can go up or down and the returns in any single year are unlikely to be 10%. From 1994 through 2022 (29 years), SPY was up in 23 years and down in 6 years. The average return in the up years was 18.5%, while the average return in the down years was -17.1%.

Source: ThoughtfulFinance.com, Bloomberg

SPY Risks

SPY owns stocks which are more volatile than cash or bonds. While the returns are higher than cash or bonds, investors need to be prepared to stomach volatility and be able to hold for the longer-term. SPY was down nearly 35% during the covid pandemic and down over 25% at one point in 2022. Looking further back, it was down nearly 50% during the 2000-2003 recession and declined over 55% during 2007-2009 recession. This is not necessarily worse than other similar funds, but it is a characteristic of stocks that investors need to be aware of.

SPY Portfolio

Fund performance is ultimately driven by a fund’s holdings and exposures, so our SPY review will examine these items.

SPY Holdings

SPY (and its underlying index) is incredibly diversified, holding over 500 stocks. This represents the large-cap segment of the US stock market.

SPY

S&P 500

Number of Stocks

503

503

Sources: ThoughtfulFinance.com, State Street (as of 4/30/2023)

SPY Country Exposures

SPY only owns US-based companies. Investors looking for international exposure may pair SPY with international ETFs or simply hold a global ETF.

SPY Market Cap Exposure

SPY is primarily a large-cap fund which seeks to represent the largest US stocks. Even though the fund holds some mid-caps, performance is primarily driven by the large-cap exposure.

SPY

Large-Cap

83%

Mid-Cap

16%

Small-Cap

0%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/22/2023

SPY Sector Exposures

SPY is extremely diversified across sectors and mirrors the approximate weights of the broad US stock market.

SPY

Basic Materials

2.27%

Consumer Cyclical

10.36%

Financial Services

12.34%

Real Estate

2.53%

Communication Services

8.75%

Energy

4.31%

Industrials

8.13%

Technology

27.43%

Consumer Defensive

7.02%

Healthcare

14.14%

Utilities

2.72%

Source: ThoughtfulFinance.com, Morningstar; data as of 5/22/2023

Expenses

No review of SPY would be complete without an in-depth look at the explicit and implicit costs of trading and holding SPY.

SPY Expense Ratio

SPY’s expense ratio of .095% is on the higher end for a large index fund, although it is still incredibly low in historical terms and compared to the rest of the market. Investors may be interested in comparing SPY vs VOO or SPY vs IVV.

SPY Transaction Costs

ETFs are free to trade at many brokers and custodians, so SPY should be free to trade in most cases. Additionally, it is among the largest ETFs and is very liquid. The bid-ask spread of SPY is about .01%, so individual investor trades will not generally be large enough to impact or move the market.

SPY Tax Efficiency

Like most index funds, SPY is very tax-efficient. Unlike actively-managed funds, passively-managed index funds typically have less trading and lower turnover. This results in fewer taxable events and higher tax efficiency.

ETFs are typically more tax-efficient than mutual funds, due to their ability to avoid realizing capital gains through like-kind redemptions (a process that is beyond the scope of this post). SPY has never made a capital gains distribution, so SPY is about as tax-efficient as any fund can be.

Investors in a high tax bracket with at least $250,000 may consider direct indexing rather than SPY, as direct indexing can potentially generate even more tax savings.

SPY Review: A Recap

The above review of SPY illustrates that SPY is a well-constructed, low-cost and tax-efficient index fund that provides diversified exposure to the US stock market. SPY is a great choice in many situations and a tool that I often use personally and professionally.

FAQs

Is SPY a good investment?

Whether SPY is a good investment or not depends on the definition of “good investment.” If the definition is something that goes up in value, then nobody knows if it is a good investment. If the definition is a well-constructed portfolio that is low-cost and will likely do what it is supposed to do (mirror the US stock market), then yes it is a good investment.

Is SPY safe long-term?

There is no way to say whether SPY or any other investment is safe long-term. SPY owns stocks, which are more volatile than cash or bonds. However, stocks have generated stronger long-term returns than cash or bonds. However, the future may unfold differently than the past, so it is impossible to say whether SPY is safe in the long-term.

Is SPY a risky investment?

SPY owns stocks, which are more volatile than cash or bonds. Some of this risk is diversified away since SPY owns hundreds of stocks, so there is not too much risk or concentration in any single stock. SPY is a well-diversified, low-cost index fund, so it is not any more risky than most stock funds.

Is SPY a buy or sell right now?

Nobody knows the future nor whether SPY is a buy or sell. SPY is an index fund and many investors use index funds because they do not believe that investors can consistently time the market or predict the ideal times to buy and sell.

Is SPY a good ETF to invest in?

The answer to this question depends on each investors’ goals. Investors looking for well-diversified, low-cost, tax-efficient exposure to the US stock market will find a lot to like in SPY. However, SPY is not a good ETF to invest in for those looking for something totally different.

Is SPY good for beginners?

For investors looking for exposure to the US stock market, SPY is not a bad choice. It can be the core position of a portfolio and provides instant diversification to investors who are building a portfolio.

Does SPY pay dividends?

Yes, SPY pays dividends. It is not necessarily a dividend-oriented fund and I would advise investors to focus on total return since dividends reduce a fund’s net asset value. In my view, receiving a dividend is equivalent to selling a small amount of the position. Investors should not focus on SPY’s dividends or dividend yield.

Which is better SPY or VTI?

SPY and VTI are slightly different. Those interested in an in-depth comparison can read my review of VTI vs SPY.

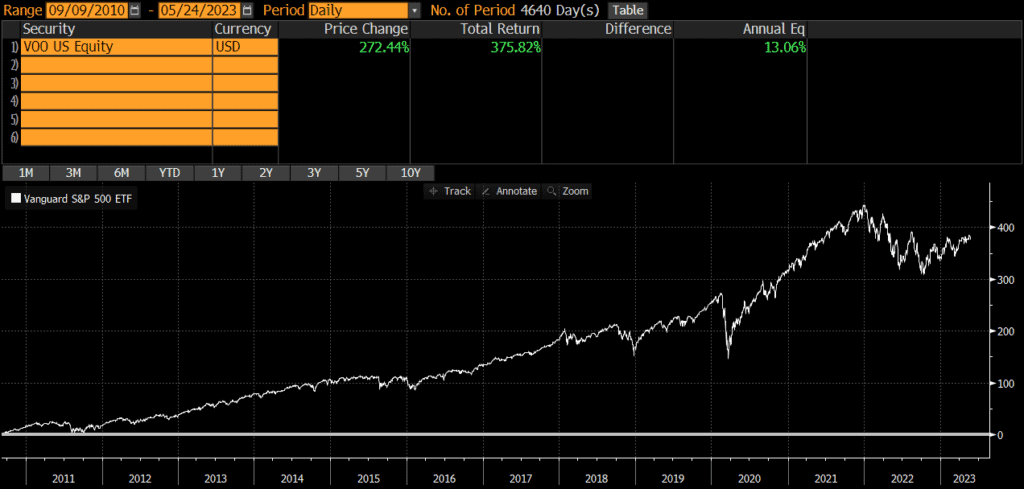

The Vanguard S&P 500 ETF (symbol: VOO) is one of the largest exchange-traded funds (ETFs) in the market and widely used by both individual and institutional investors. VOO is a low-cost index fund, which tracks the S&P 500 Index. The fund seeks to provide exposure to the US stock market at a very low price. The fund is the core of many portfolios and the below review of VOO will evaluate why that is.

The first thing most investors want to know about is performance, so we will start there. According to Bloomberg, since the fund’s inception 13 years ago, VOO has returned over 13% per year. Of course, this figure can go up or down and the returns in any single year are unlikely to be 13%. From 2011 through 2022 (12 years), VOO was up in 10 years and down in 2 years. The average return in the up years was 17.8%, while the average return in the down years was -11.34%.

Source: ThoughtfulFinance.com, Bloomberg

VOO Risks

VOO owns stocks which are more volatile than cash or bonds. While the returns are higher than cash or bonds, investors need to be prepared to stomach volatility and be able to hold for the longer-term. VOO was down nearly 35% during the covid pandemic and down over 25% at one point in 2022. This is not necessarily worse than other similar funds, but it is a characteristic of stocks that investors need to be aware of.

VOO Portfolio

Fund performance is ultimately driven by a fund’s holdings and exposures, so our VOO review will examine these items.

VOO Holdings

VOO (and its underlying index) is incredibly diversified, holding over 500 stocks. This represents the large-cap segment of the US stock market.

VOO

S&P 500

Number of Stocks

505

503

Sources: ThoughtfulFinance.com, Vanguard (as of 4/30/2023)

VOO Country Exposures

VOO only owns US-based companies. Investors looking for international exposure may pair VOO with international ETFs or simply hold a global ETF.

VOO Market Cap Exposure

VOO is primarily a large-cap fund which seeks to represent the largest US stocks. Even though the fund holds some mid-caps, performance is primarily driven by the large-cap exposure.

VOO

Large-Cap

83%

Mid-Cap

17%

Small-Cap

0%

Source: ThoughtfulFinance.com, Morningstar; data as of 04/30/2023

VOO Sector Exposures

VOO is extremely diversified across sectors and mirrors the approximate weights of the broad US stock market.

VOO

Basic Materials

2.35%

Consumer Cyclical

10.17%

Financial Services

12.59%

Real Estate

2.62%

Communication Services

8.28%

Energy

4.69%

Industrials

8.18%

Technology

26.42%

Consumer Defensive

7.32%

Healthcare

14.49%

Utilities

2.88%

Source: ThoughtfulFinance.com, Morningstar; data as of 4/30/2023

Expenses

No review of VOO would be complete without an in-depth look at the explicit and implicit costs of trading and holding VOO.

VOO Expense Ratio