MSCI ACWI ex-US vs MSCI ACWI ex-US IMI (Investable Market Index)

The MSCI ACWI ex-US Index and the MSCI ACWI ex-US IMI (Index Investable Market Index) are two of the most followed global stock indices that exclude the US. Many portfolios and investment vehicles are benchmarked to each index.

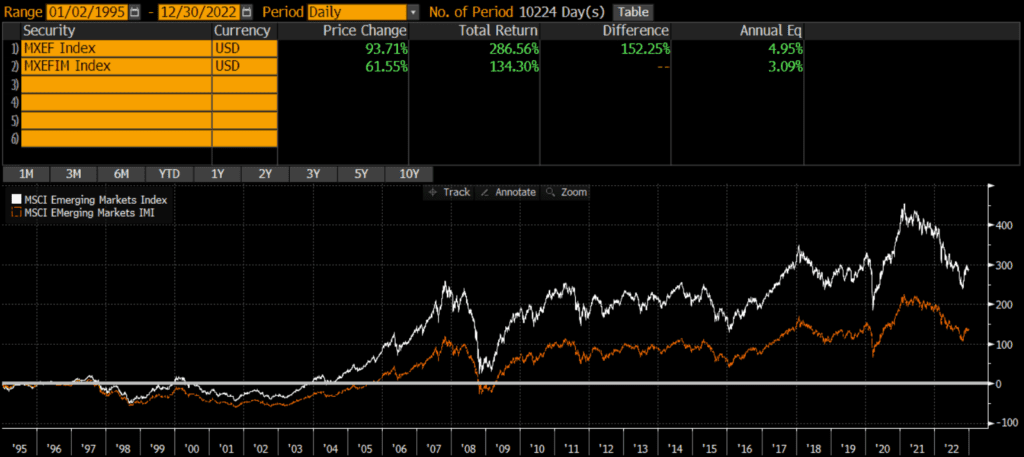

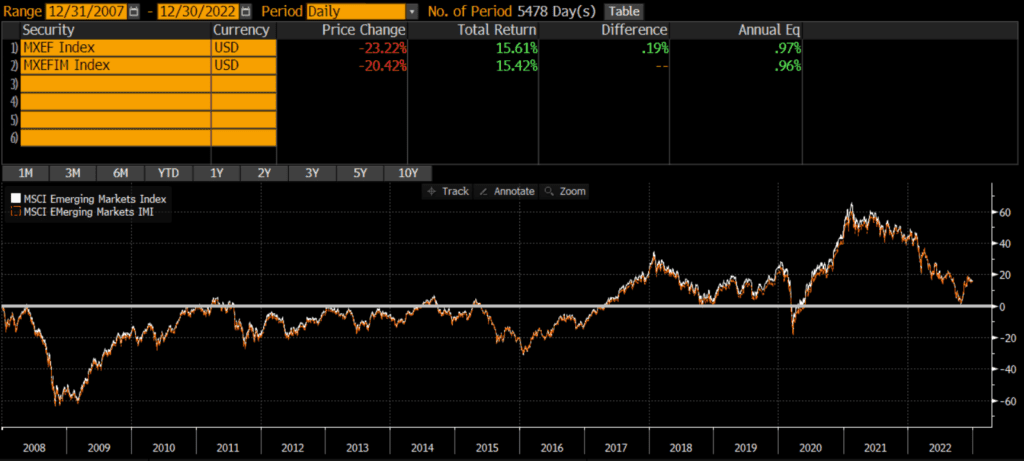

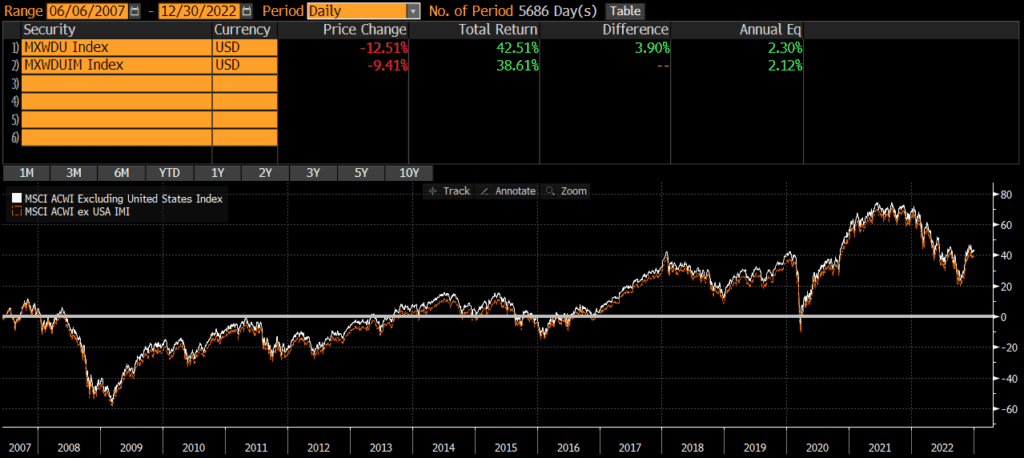

The MSCI ACWI ex-US Index and the MSCI ACWI ex-US IMI have some slight differences, but performance has been nearly identical. The below performance chart of the MSCI ACWI ex-US and MSCI ACWI ex-US IMI illustrates that the MSCI ACWI ex-US Index has outperformed the IMI version on a backtested basis. However, returns since the MSCI EM IMI’s inception have been nearly identical. This similar to the findings in my analysis of the Russell 1000 vs S&P 500 and MSCI EM vs MSCI EM IMI.

A quick note that investors cannot invest directly in an index. These unmanaged indexes do not reflect management fees and transaction costs that are associated with an investable vehicle, such as the iShares ACWI ex-US ETF (symbol: ACWX) or the iShares Core MSCI Total International Stock ETF (symbol: IXUS). A reminder that these are simply examples as this site does NOT provide investment recommendations.

What is the difference between MSCI ACWI ex-US and MSCI ACWI ex-US IMI?

The MSCI ACWI ex-US IMI (Investable Market Index) is similar to the traditional MSCI ACWI ex-US Index (non-IMI), but it has many more constituent stocks and includes more exposure to mid-caps and small-caps.

What is MSCI ACWI ex-USA IMI index?

The IMI in “MSCI ACWI ex-US IMI” stands for “Investable Market Index” and connotes that it includes more stocks than the original ACWI ex-US index.

Historical Performance: MSCI ACWI ex-US vs MSCI ACWI ex-US IMI

The MSCI ACWI ex-US Index was launched in 1995, while the MSCI ACWI ex-US IMI Index was launched 22 years later on June 5, 2007. Since inception, performance has been nearly identical. The MSCI ACWI ex-US has outperformed the MSCI ACWI ex-US IMI by .18% per year (2.30% vs 2.12%, respectively). The cumulative performance differential over that time period has been over 4%!

Composition Differences: MSCI ACWI ex-US vs MSCI ACWI ex-US IMI

Both the MSCI ACWI ex-US vs MSCI ACWI ex-US IMI indices are broad-based indices that represent the equity markets of developed nations. As of 12/31/2022, the indices have similar geographic exposures, similar sector weights, and slightly different market cap exposures.

Geography

The MSCI ACWI ex-US index and the ACWI ex-US IMI have identical country constituents, although the weight vary ever so slightly. Below are the weights of the top five countries.

| MSCI ACWI ex-US Index | MSCI ACWI ex-US Investable Market Index | |

| Japan | 14.03% | 15.01% |

| United Kingdom | 9.76% | 9.79% |

| China | 9.16% | 8.25% |

| Canada | 7.72% | 7.67% |

| France | 7.57% | 6.86% |

Market Capitalization

One of the main differences between the two indices is that the MSCI ACWI ex-US Investable Market Index (IMI) has many more constituents that the original MSCI ACWI ex-US Index. According to MSCI, the number of constituents is as follows:

| MSCI ACWI ex-US Index | MSCI ACWI ex-US IMI Index | |

| Constituent Stocks | 2,261 | 6,592 |

Additionally, the two indices have slightly different market cap exposures. Using the iShares ACWI ex-US ETF (which tracks the MSCI ACWI ex-US Index) (symbol ACWI ex-US) and the State Street SPDR Portfolio MSCI Global Stock ETF (which tracks the MSCI ACWI ex-US IMI Index) (symbol SPGM) as proxies, we can infer the below market cap weights of each index.

| MSCI ACWI ex-US Index | MSCI ACWI ex-US IMI Index | |

| Large Cap | 88% | 77% |

| Mid Cap | 12% | 19% |

| Small Cap | 0% | 4% |

Sector Weights

Again, using ACWX and IXUS as proxies, we can infer the index weights are very similar.

| MSCI ACWI ex-US IMI | MSCI ACWI ex-US Index | |

| Basic Materials | 8.51% | 8.85% |

| Consumer Cyclical | 11.19% | 11.40% |

| Financial Services | 20.91% | 19.42% |

| Real Estate | 2.32% | 3.35% |

| Communication Services | 6.42% | 6.06% |

| Energy | 5.93% | 5.64% |

| Industrials | 12.07% | 13.27% |

| Technology | 11.33% | 11.29% |

| Consumer Defensive | 8.47% | 8.12% |

| Healthcare | 9.77% | 9.49% |

| Utilities | 3.06% | 3.12% |

Final Thoughts on MSCI ACWI ex-US Index vs ACWI ex-US IMI

Investors cannot invest in indices directly and should do their own research before deciding to invest in a fund that tracks either index. That being said, these two indices appear nearly identical in terms of geographic, market cap, and sector exposure. For all intents and purposes, I would argue that these two benchmarks are interchangeable.

With such a small performance difference, the costs of actual investment strategies/vehicles may be a larger consideration than which benchmark to select. Sometimes benchmark selection matters quite a bit, although that does not appear to be the case between these two indices.