Hi, I’m Matt. Most of my time is spent managing an investment advisory firm.

Helping people reach their goals through investing is incredibly satisfying. Yet my firm can only serve so many clients, many investors do not have enough assets to work with an investment advisor, and I recognize that some people prefer to manage their own investments even if they can work with an advisor.

My goal is to provide readers with the resources that they need to reach their own goals.

Several years ago, I wrote a two-part guest post about marketplace lending as an investment asset class. It has been truly amazing to watch the industry’s growth and see how widely marketplace lending is now accepted as a bona fide asset class. The industry’s maturation has mitigated many risks, but I also believe that the rapid growth and increasing competition has increased other risks.

The primary risks today, in my opinion, stem from the decline in lending rates. Although rates were declining in 2013 (when I first invested in and wrote about marketplace loans), rates were much higher then. Today, rates have already come down significantly and continue to decline. Lower projected returns translate to a narrower margin of safety. Many, if not all, of the below risks have existed for quite some time and have been widely expected at some point, but they warrant more caution now due to today’s lower and still-declining rates.

Loan Refinancing

One factor that has been driving down returns has been loan refinancings, which represent a conflict of interest between investors and the platforms. Investors would generally prefer to hold performing loans to maturity in order to maximize returns, whereas the platforms are incentivized to originate as many loans as possible in order to maximize revenue. These are not mutually exclusive interests, but the platforms have been actively soliciting existing borrowers to refinance their loans at lower rates for the past several years. This is not inherently wrong (it’s great for borrowers), but investors should realize that a conflict of interest exists and that their loans are callable at any time (which is detrimental during a period of declining rates, since reinvestment returns will be lower). Orchard Platform recently posted a good summary of this issue here.

Loan Quality Questions

As more platforms go public, the pressure to grow continues to increase. Growing loan volume needs to be carefully weighed against maintaining loan quality. My observation is that both the pressure to grow and the huge demand for loans has led to a loosening of underwriting standards. We are seeing explicit examples, such as “high yield” offerings and euphemistically named “near prime” loans. But several sources have also confirmed that at least some platforms are now accepting less borrower documentation than they have in the past. My hope is that the technology used in place of traditional underwriting methods is robust enough to make up for the weaker verification processes. Only time will tell.

Questionable Practices in the Corners of Business Lending

The 2015 LendIt conference in New York (highly recommended!) was a great showcase of the industry and I met a ton of interesting people and learned about many marketplace lending platforms that focus on business lending. However, a few of the business lending platforms and funds were extremely aggressive. I am not trying to be moralistic, but it was honesty difficult to tell whether some of the platforms were helping or exploiting borrowers. A more economic concern is that several claimed that their high-degree of collateralization mitigated a lot of risk, but further questioning about recovery rates called many of these claims into question. This certainly does not apply to the entire business lending segment, but I would encourage investors to research any platform and/or manager that they are considering.

Investor Risk Analysis

The platforms’ risk models appear much more robust, but my guess is that many individual investors rely on some of the public commentary that compares the credit risks of marketplace lending with the credit risks of credit cards. This is an imperfect analog, at best, since revolving consumer credit (like credit cards) is fundamentally different from non-revolving personal loans (like marketplace lending) on many levels. For instance, a troubled credit card customer has an incentive to continue paying their monthly bill so that they can continue to use the card. A marketplace lending borrower does not have that incentive. This is not a prediction that marketplace loan loss rates will exceed credit card loss rates in the next economic downturn (although they may), but I would encourage investors to consider possible losses carefully.

Conclusion

As “peer-to-peer lending” matures towards “marketplace lending,” the high returns of early-adopters are now trending down towards market-driven ones. I believe marketplace lending will provide positive returns for quite some time, but the margin of safety is narrowing and its relative value to other investable markets has diminished as well. My hope is that all parties protect the integrity of the asset class, to ensure its long-term viability. Of course, hope is not a prudent investment strategy, which is why I am writing this and encourage all marketplace lending investors to recognize and weigh the risks along with the opportunity.

Full Disclosure: I advise clients on private investment vehicles dedicated to the marketplace lending asset class, as well as personally own loans on both the Lending Club and Prosper platform. I am also a client of NSR Invest.

Just as Michael Milken found that junk bond rates in the 1980’s were sufficiently high to buffer against the losses from defaults, I see the same favorable dynamic in P2P lending today. P2P has higher rates, defaults, and total returns than many other types of fixed-income today. Drilling down within P2P lending, we find that higher-grade notes have fewer defaults, while “riskier” notes have higher returns (again, because the higher rates are more than sufficient to cover the losses from higher defaults).

While some commentators may dismiss P2P as an asset class, due to the higher default rates, we know that price (or yield) is the arbiter of risk and so we need to examine whether P2P compensates investors for the risk taken. Whether we define risk as an unknown outcome or the probability of loss, we need to quantify it. For simplicity’s sake, lets run a portfolio of notes through several scenarios.

Best Case: We could assume the status quo continues, which is to say consumer finances are improving and defaults remain low. Loss-adjusted returns may average 4-5% on a high-grade portfolio, 8-9% for a broad-based portfolio, and 11-13% for a low-grade portfolio.

Worst Case: In a worst-case scenario, á la 2008-2009 recession which saw unemployment surge and consumer balance sheets decimated, we learned a couple of things. If you look at data on all Lending Club notes, as well as independent analysis on sites like NickelSteamroller.com or LendStats.com, the only year in which total originations had a negative return was 2007. Of course, there was some pretty horrific performance out of loans originated during the fall and winter of 2008-2009. I do not have space to detail the composition, timing, and other more granular aspects of the recession performance, but this data can easily be pulled from the aforementioned sources.

Prosper notes had significantly worse losses during the recession, although I believe much of this is attributable to their early practice of allowing participants to set rates. This taught us that skilled and professional underwriting is essential to maintaining the integrity of P2P product. Furthermore, it supports (but does not prove) that originator-set rates/prices ensure P2P investing is a profitable experience.

Anyone can create their own stress-test by assuming higher default rates, but I am content to use the historical stress-test of the 2008-2009 recession. I should mention that it would be prudent for anyone using a historical or hypothetical stress-test to take into account the many changes made on Lending Club’s platform since 2007, some of which may improve returns and some which might reduce them.

Similar to interest rate risk, the credit risk of P2P loans compares favorably with other fixed-income assets. It is possible the US could experience another recession, perhaps even a deep one. If you only buy the riskiest notes during the worst months, you are definitely hosed (that’s a sophisticated institutional term). However, this would be hard to do even if you tried; if you diversify across grades and vintages, P2P is an attractive asset class.

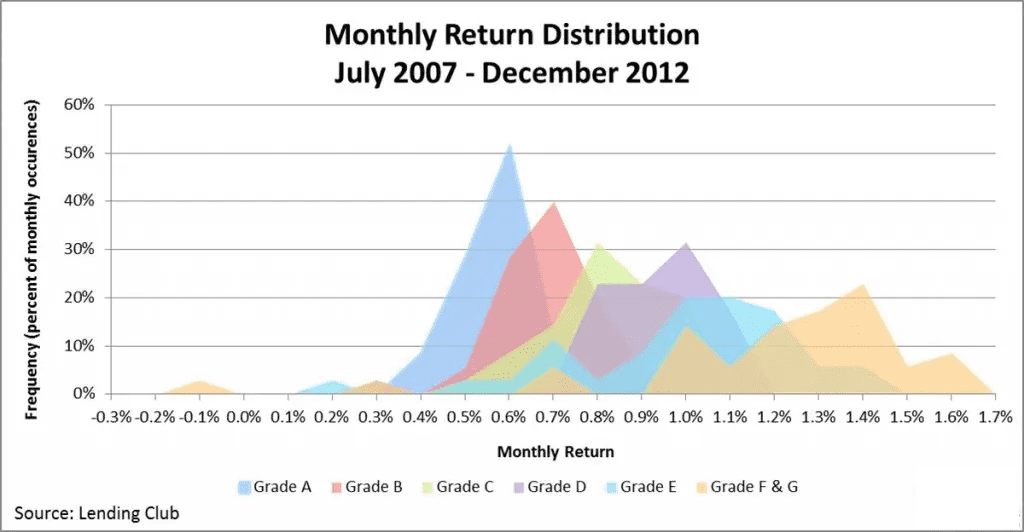

Below are the monthly return distributions of all Lending Club notes, since inception, sorted by grade:

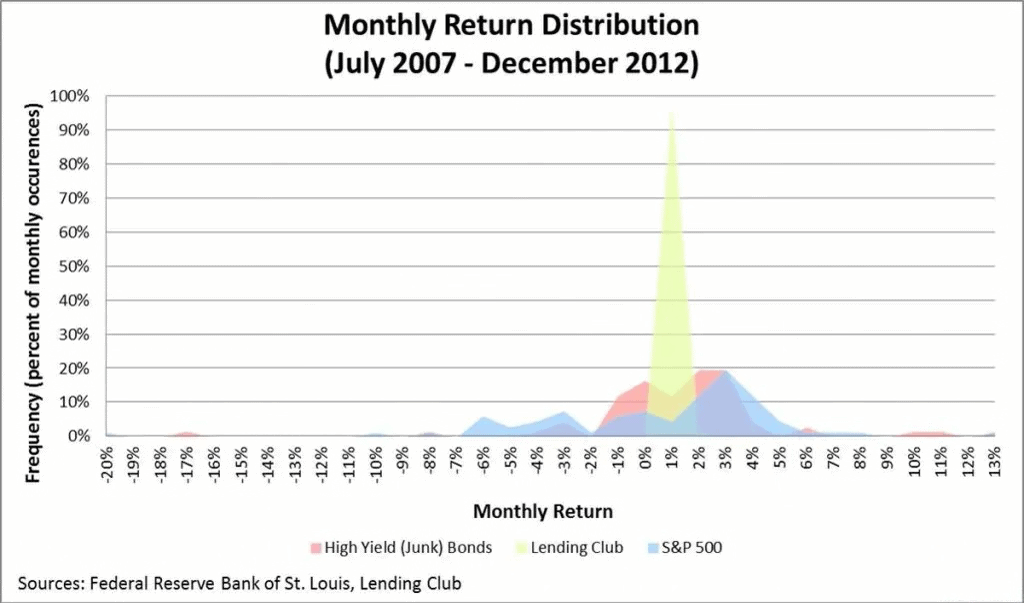

And here are the monthly return distributions for all Lending Club loans, since inception, relative to high yield bonds and the S&P 500 over the same timeframe. Notice the x-axis scale when comparing the two charts…

One last consideration is to understand where your credit risk exposure is. Typically, an ABS sponsor establishes a separate entity, called a special purpose vehicle (SPV), to buy and hold the loans and issue securities to investors. The SPV is considered “bankruptcy remote” from the sponsor, which means the loans are protected should the sponsor go bankrupt.

Prosper has established an SPV, called Prosper Funding. Prosper Marketplace (the service side) originates the loans, transfers them to Prosper Funding, who then issues the notes to investors. So investor assets are held in Prosper Funding, which is distinct from Prosper Marketplace; thus, in a hypothetical Prosper Marketplace bankruptcy, creditors should not be able to recover the loans/notes from investors.

Lending Club, on the other hand, holds the loans/notes on its balance sheet. According to the most recent prospectus, if Lending Club went bankrupt, then note holders would be considered unsecured creditors of Lending Club (not of the borrowers). Basically, investors are lending money to Lending Club, who originates and owns the loans and promises to pass the principal and interest payments back to the investors. So investors do not technically own the notes, as Lending Club states in its prospectus, and it is important to note that you are ultimately exposed to Lending Club’s credit risk (as well as the borrowers’). Given the current financial position of Lending Club, I am not too concerned about the lack of an SPV, but it is worth mentioning and investors should monitor Lending Club’s balance sheet regularly.

Interest Rate Risk

Since all P2P loans are short-term (3 or 5 years), are fully amortizing, and have relatively high coupon rates, duration (a measure of interest rate risk) on any given note is extremely low. I believe that the duration for any given note may even overstate many notes’ price sensitivity to interest rates, since the secondary market is not yet mature. It would be interesting to analyze Foliofn data for the past two months and see if secondary market prices dropped significantly in response to the rally in rates. Regardless, the interest rate risk is miniscule, which is ideal for times like these.

However, even if price fluctuations from rising rates are minimal, owning fixed-income in a rising rate environment creates an opportunity cost. This is because the rates on new loans will be higher than the rates on the loans you own. While I have read some research showing that 36-month loans have less credit risk than 60-month loans, I have not seen anyone mention the fact that there is a much lower opportunity cost to holding a 36-month loan, should interest rates rise. If rates rise, I assume the P2P originators will raise their lending rates. A shorter loan term will return your principal more quickly, which means you can reinvest it at higher rates sooner. Lastly, like many asset-backed securities (ABS), P2P loans have an average life that is shorter than their stated maturity, due to the borrower prepayment option. This further reduces the opportunity cost if rates rise (although this would be called “call risk” in a falling rate environment).

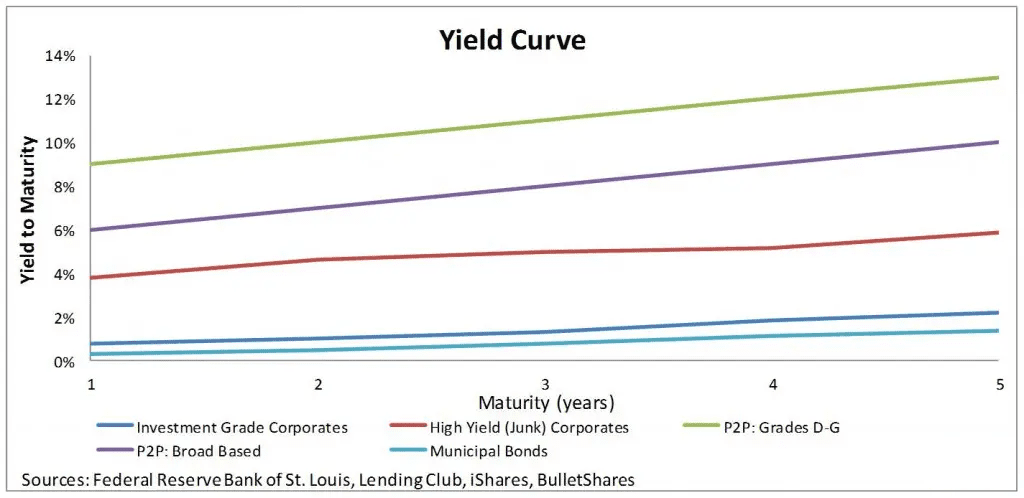

Looking around the rest of the fixed-income market, we find 2-year Treasuries yielding .26%, most 2-year investment-grade corporate bonds below 1%, and 2-year high-yield corporates in the 4-5% range. A 36-month P2P note has a similar duration to a 2 year bullet bond, but offers a much higher yield than all of these:

P2P Risks

Beyond the risks common to all fixed income, the two P2P-specific risks I see involve the withdrawal of P2P’s competitive advantages: solid underwriting/risk-management and originator-set rates.

As we saw with investment bankers during the dotcom bubble and mortgage bankers during the housing boom, it is always dangerous to incentivize the origination of investment products, especially if the originators do not intend to hold product on their books. Although the P2P originators collect a 1% servicing fee, the majority of their revenue comes from loan origination fees. It is important to recognize this fact and monitor any changes to the underwriting standards.

Secondly, as noted previously, the fact that the originators are setting the prices/yields and shielding the offering prices from market prices mean that excess returns are available. If this changes in any way, I would be very cautious as this is the crux of the P2P value proposition.

Conclusion

In summary, I do think P2P is a viable fixed-income asset class, with a unique advantage over similar ABS and high-yield debt. Given current dynamics, I think most fixed-income portfolios should include an allocation to P2P loans. Interest rate risk is almost non-existent and there is more than enough yield to cover the credit risk, except under the most dire scenarios. That said, I believe the asset class proved itself through the recent recession, relative to other debt. Investability (especially in size) remains an issue, although that is another blog post. Nevertheless, for this reason, P2P investing is an asset class in which individual investors can outperform the larger institutional investors due to the small size of the current P2P market. Of course, I suggest they borrow some of the tools from traditional fixed-income investment management to refine their strategies.

Much of the discourse and analysis surrounding peer-to-peer (P2P) lending and investing has been written by, and targets, individual investors. Although there are institutional investors in the space, P2P is still largely ignored as it is a relatively small, misunderstood, and difficult-to-access asset class. Thus, the purpose of this article is two-fold. Firstly, I hope to consolidate some of the commentary out there to place P2P lending into a standardized fixed-income framework and, secondly, use this framework to make a case for P2P lending.

First, some terminology:

P2P Originators or P2P Sponsors: Lending Club and Prosper, among others.

“Price” and “Yield” are used interchangeably, as they are opposite sides of the same coin. Generally, price and yield always move inversely to each other. I have tried to use both where applicable and possible.

Excess Return: Expected return above that of another investment of similar risk. Other definitions do exist though.

Asset-Backed Security (ABS): Type of bond most analogous to a portfolio of P2P notes. ABS are usually backed by aggregated financial assets like loans or leases. To be clear, the claim on the future cashflows is the asset (think accounting assets, not a physical asset). Usually, they are consumer loans (like credit cards or student loans) and are sometimes collateralized (such as auto loans or home equity loans).

P2P Lending Through a Fixed-Income Lens

Ever since I heard about P2P lending, I have enjoyed reading blogs on the subject (such as this one) and individuals’ accounts of their experiences with P2P. An interesting pattern, though, has been to read someone’s observations, discoveries, and/or theories which are brand new to them (or even the P2P community) but are well-known concepts in the field of fixed-income investing. I think this is exciting in that the process of discovery is always thrilling, but also an opportunity for more education and learning for P2P investors; they do not need to reinvent the wheel. By utilizing traditional fixed-income tools, P2P investors can better quantify and manage risks and returns.

For instance, many people (maybe less so now that the asset class is a bit older and has more literature) who share their P2P investing strategies make a sudden shift at some point, from focusing on minimizing defaults to focusing on maximizing returns. Usually, this takes the form of, “I used to invest solely in grades ___ and above, but now only invest in grades D and below.” The idea that minimizing bond defaults does not necessarily lead to higher returns was discovered in the 1980’s, which is to say that it was both a major discovery (in such an old market) and also already known before the advent of P2P lending in the 2000s.

Just 30 years ago, professional fixed-income managers evaluated bonds on an individual basis, much as some P2P investors do who read each loan description and try to judge the likelihood of default. Back then, bonds whose credit rating dropped below investment-grade were summarily sold, as the risk of holding them was deemed too high. In the 1980’s, Michael Milken (then the “Junk Bond King,” later a convicted felon, and now a prolific philanthropist) discovered that while “junk bonds” (those rated below investment-grade) were individually risky, they were so uniformly underpriced (meaning that yields were high) that a diversified portfolio of them could do much better than an investment grade portfolio with lower default rates. Statistically, the returns from higher rates should more than offset the losses of expected defaults.

The P2P originators and countless websites enumerate the many characteristics and benefits of P2P investing. Most align with one of the following concepts.

Match borrowers and savers, but cut out the “middle man” (mainly banks)

Transparent borrower and underwriting data

Consistent cash flow

Lowered risk from diversification benefits

Secondary market liquidity

High yields

Each of these attributes apply to nearly all fixed-income products, except that the yields in P2P investing today are much higher than in other markets. Initially I was very skeptical of the performance claims relating to P2P lending, as the returns seemed much too high for what is essentially an asset-backed security (ABS). However, upon further due diligence, I found P2P investing possesses a single idiosyncrasy which sets it apart from traditional ABS and other fixed-income vehicles and is responsible for the attractive returns. Without this feature, I do not think P2P lending would produce high returns or attract much investor interest.

The P2P Opportunity

I have seen many investments promise high returns or yields, only to learn they are highly leveraged, have volatile cash flows, or use creative methodology/definitions when calculating “yield.” If any investment is offering a high return potential, my first question (and perhaps yours) is always, “Why haven’t other investors already jumped in and bid up the price (driven down the yield) to a level where it no longer offers excess return?” Although there are many characteristics that make P2P lending a legitimate asset class, the main factor that sets it apart from other fixed-income asset classes and drives the much higher returns is the fact that P2P originators set the price instead of the market. In most other fixed-income markets, the offering price (yield) is set by the market either directly or indirectly. Typically, if something is underpriced and offering superior risk-adjusted returns, it will be bid up to a price where it no longer offers a superior return.

For example, when the US Treasury issues Treasury bills, notes, and bonds, it holds an auction. Prospective buyers submit a bid stating the lowest yield that they are willing to accept. The Treasury then sells the debt to each bidder, from lowest acceptable yield to highest, until the prescribed amount of debt is sold (all buyers get the same price, which is the highest yield). Similarly, when many corporate bonds are issued, the underwriters look to the secondary market to determine pricing, as that is a good indication of what people are willing to pay for a new offering. This would be akin to the P2P originators using data from recent Foliofn transactions to set prices/yields on new loans. As many of you know, the average yields on Foliofn are a bit lower (prices are higher) than buying directly from the originators.

I believe P2P represents an excellent investment opportunity as long as this pricing structure remains in place. For the time being, returns (prices) are above (below) where market participants would transact, leading to excess returns and more demand for than supply of loans. The originators have publicly stated that they are focused on originating quality product to keep investors happy and returning. However, I can envision price/yield changes being made down the road to remedy the supply/demand imbalance or to increase loan volume. However this does not seem to be a near-term risk. There are a myriad of risks to consider in fixed-income investing, from macro themes like inflation to market concerns like liquidity.

In tomorrow’s post we will focus on the two main risks in fixed-income: credit risk and interest rate risk and how they apply to P2P.