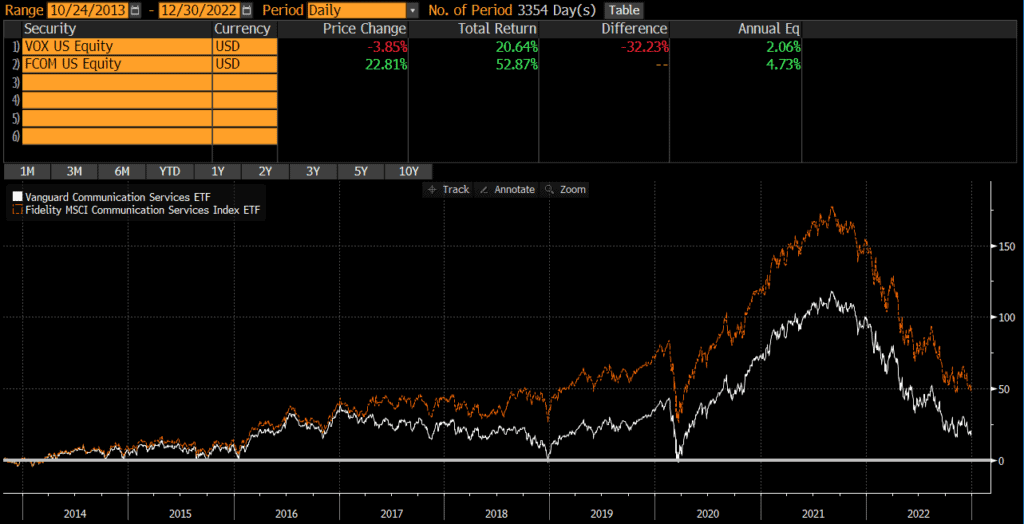

VOX vs XLC

The Vanguard Communication Services Index Fund ETF (VOX) and State Street’s The Communication Services Select Sector SPDR Fund (XLC) are two of the largest communication services sector ETFs and two of the most popular among individual investors. Many investors compare VOX vs XLC because they are so similar. The funds are quite similar with one important difference.

A quick reminder that this site does NOT provide investment recommendations. Fund comparisons (such as this one) are not conducted to identify the “best” fund (since that will vary from investor to investor based on investor-specific factors). Rather, these fund comparison posts are designed to identify and distinguish between the fund details that matter versus the ones that don’t.

The Short Answer

The primary difference between these funds is that XLC is a large-cap fund, while VOX includes more mid-caps and small-caps.

The Longer Answer

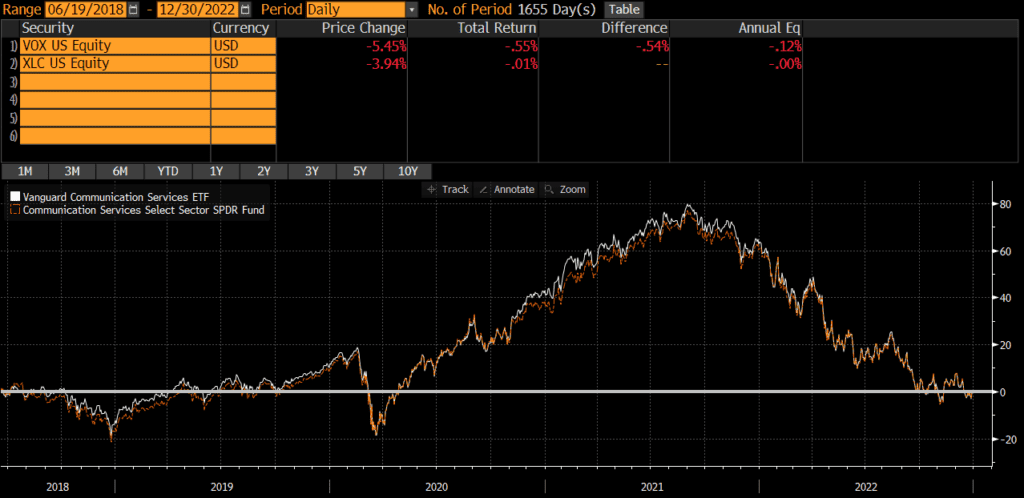

Historical Performance: VOX vs XLC

VOX was launched back in 2004, while XLC was launched in 2018 (when many index providers spun several major communication services stocks out of the information technology sector). Since the XLC’s launch, the two funds have performed nearly identically, with an annualized difference of only .12%!

Portfolio Exposures: VOX vs XLC

XLC tracks the Communication Services Select Sector Index, which is essentially a sub-index of the S&P 500 (which is predominantly composed of large-caps). It has changed over the years, but the index that VOX currently tracks is includes more mid-caps and small-caps.

Geographic Exposure

Both VOX and XLC hold essentially 100% stocks, so I will not dig into country exposures or market classification here. For all intents and purposes, the two funds have identical geographic exposures.

Market Cap Exposure

As the below data illustrates, XLC primarily holds large-caps, while VOX holds more mid-caps and includes small-caps. Despite this difference, both funds are market-cap weighted and risk/return is overwhelmingly driven by the large-cap exposure.

| XLC | VOX | |

| Large Cap | 80% | 67% |

| Mid Cap | 19% | 22% |

| Small Cap | 0% | 10% |

Sector Exposure

VOX and XLC are communication services ETFs and so their holdings are 100% communication services stocks.

Practical Factors: VOX vs XLC

Transaction Costs

As ETFs, both XLC and VOX are free to trade on many platforms. Bid-ask spreads for both VOX and XLC are extremely low and volume is sufficient to prevent most individual investors from “moving the market.” Investors looking for an ETF version of VOX should read my post comparing VOX and VTCAX.

Expenses

The expense ratio for both XLC and VOX is .10%. At these low levels of expense ratios, small differences in expense ratios does not typically matter anyways. Something to keep in mind if one fund or the other decides to reduce fees.

Tax Efficiency & Capital Gain Distributions

Neither VOX nor XLC has ever made a capital gain distribution and I do not expect either fund to make capital gains distributions moving forward (since they are ETFs). In my opinion, these two funds are equally tax-efficient.

Options Strategies

The one factor that may sway someone towards XLC is if they are managing some type of option strategy, such as covered calls. The options market for XLC is much more active than for VOX. Of course, if someone wants to trade options without triggering tax consequences in another part of their portfolio, perhaps VOX is the better pick for the non-option holding.

Bottom Line: VOX vs XLC

Given XLC’s short history, it may be too early to say, but VOX and XLC appear identical in nearly every way and I would not spend too much time comparing them or trying to decide which is better. I believe investors’ time is better spent evaluating and thinking through more material decisions.

Investors may also want to read my comparison of VOX vs FCOM (Fidelity’s communication services ETF).