The Vanguard Consumer Staples Index Fund ETF (VDC) and the Fidelity MSCI Consumer Staples Index ETF (FSTA) are two of the largest consumer staples sector ETFs and two of the most popular among individual investors. Many investors compare VDC vs FSTA because they are so similar, although differences are difficult to find.

A quick reminder that this site does NOT provide investment recommendations. Fund comparisons (such as this one) are not conducted to identify the “best” fund (since that will vary from investor to investor based on investor-specific factors). Rather, these fund comparison posts are designed to identify and distinguish between the fund details that matter versus the ones that don’t.

The Short Answer

VDC and FSTA track the same index and there is no material difference between the funds. They are identical and interchangeable in my opinion.

The Longer Answer

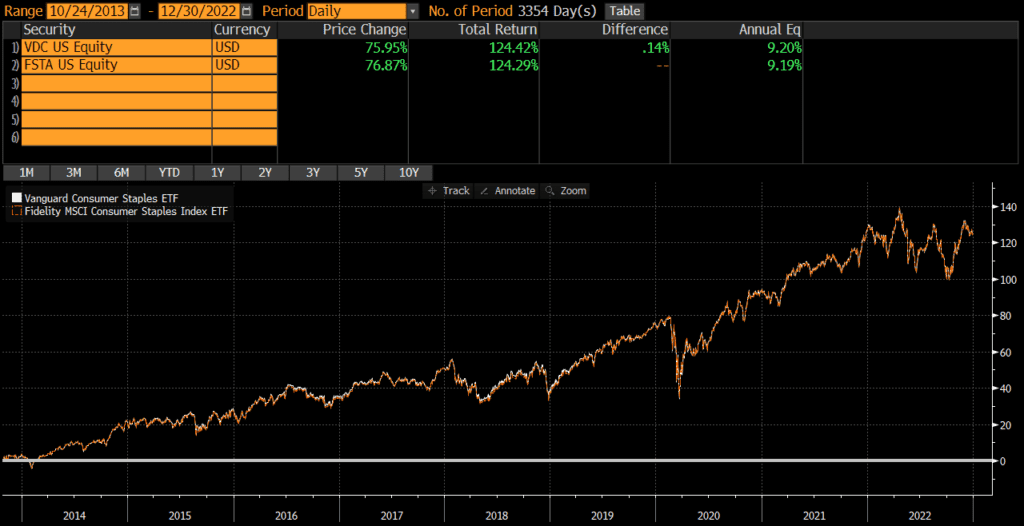

Historical Performance: VDC vs FSTA

VDC was launched back in 2004, while FSTA was launched on October 21, 2013. Since then, the two funds have performed identically, with an annualized difference of only .01%! The cumulative performance differential over that timeframe has only been .14% too! From a performance perspective, VDC and FSTA are identical and interchangeable.

Portfolio Exposures: VDC vs FSTA

Both VDC and FSTA track the same index, the MSCI US Investable Market Consumer Staples 25/50 Index. Consequently, the two funds have identical geographic, market-cap, and industry exposures.

Geographic Exposure

Both VDC and FSTA hold essentially 100% stocks, so I will not dig into country exposures or market classification here. For all intents and purposes, the two funds have identical geographic exposures.

Market Cap Exposure

As mentioned above, both funds track the same index and have materially identical market cap exposures.

Sector Exposure

VDC and FSTA are consumer staples ETFs and so their holdings are 100% consumer staples stocks.

Practical Factors: VDC vs FSTA

Transaction Costs

As ETFs, both FSTA and VDC are free to trade on many platforms. Bid-ask spreads for both VDC and FSTA are extremely low and volume is sufficient to prevent most individual investors from “moving the market.”

Expenses

FSTA has a lower expense ratio at .08%, compared to VDC’s .10%. Although VDC is 25% more expensive, we’re talking about 2 basis points. At these low levels of expense ratios, the difference doesn’t matter.

Tax Efficiency & Capital Gain Distributions

VDC has not made a capital gains distribution since 2004 and I do not expect it to make any moving forward. FSTA has never made a capital gain distribution. In my opinion, these two funds are equally tax-efficient.

From a tax-loss harvesting perspective, investors may want to avoid using these two funds as substitutes for one another since they could be considered “substantially identical” (given that they track the same index and are identical in many ways).

Bottom Line: VDC vs FSTA

VDC and FSTA are identical in nearly every way. I would not spend any time comparing them or trying to decide which is better.

Investors interested in other consumer staple ETFs may want to check out my comparison of VDC vs XLP (State Street’s consumer staple ETF). Investors looking for a mutual fund should read my post of VDC’s mutual fund share class VCSAX.